如果你也在 怎样代写时间序列Time Series EMET3007/8012这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。时间序列Time Series是在数学中,是按时间顺序索引(或列出或绘制)的一系列数据点。最常见的是,一个时间序列是在连续的等距的时间点上的一个序列。因此,它是一个离散时间数据的序列。时间序列的例子有海洋潮汐的高度、太阳黑子的数量和道琼斯工业平均指数的每日收盘值。

时间序列Time Series分析包括分析时间序列数据的方法,以提取有意义的统计数据和数据的其他特征。时间序列预测是使用一个模型来预测基于先前观察到的值的未来值。虽然经常采用回归分析的方式来测试一个或多个不同时间序列之间的关系,但这种类型的分析通常不被称为 “时间序列分析”,它特别指的是单一序列中不同时间点之间的关系。中断的时间序列分析是用来检测一个时间序列从之前到之后的演变变化,这种变化可能会影响基础变量。

时间序列Time Series代写,免费提交作业要求, 满意后付款,成绩80\%以下全额退款,安全省心无顾虑。专业硕 博写手团队,所有订单可靠准时,保证 100% 原创。最高质量的时间序列Time Series作业代写,服务覆盖北美、欧洲、澳洲等 国家。 在代写价格方面,考虑到同学们的经济条件,在保障代写质量的前提下,我们为客户提供最合理的价格。 由于作业种类很多,同时其中的大部分作业在字数上都没有具体要求,因此时间序列Time Series作业代写的价格不固定。通常在专家查看完作业要求之后会给出报价。作业难度和截止日期对价格也有很大的影响。

同学们在留学期间,都对各式各样的作业考试很是头疼,如果你无从下手,不如考虑my-assignmentexpert™!

my-assignmentexpert™提供最专业的一站式服务:Essay代写,Dissertation代写,Assignment代写,Paper代写,Proposal代写,Proposal代写,Literature Review代写,Online Course,Exam代考等等。my-assignmentexpert™专注为留学生提供Essay代写服务,拥有各个专业的博硕教师团队帮您代写,免费修改及辅导,保证成果完成的效率和质量。同时有多家检测平台帐号,包括Turnitin高级账户,检测论文不会留痕,写好后检测修改,放心可靠,经得起任何考验!

想知道您作业确定的价格吗? 免费下单以相关学科的专家能了解具体的要求之后在1-3个小时就提出价格。专家的 报价比上列的价格能便宜好几倍。

我们在统计Statistics代写方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计Statistics代写服务。我们的专家在时间序列Time Series代写方面经验极为丰富,各种时间序列Time Series相关的作业也就用不着说。

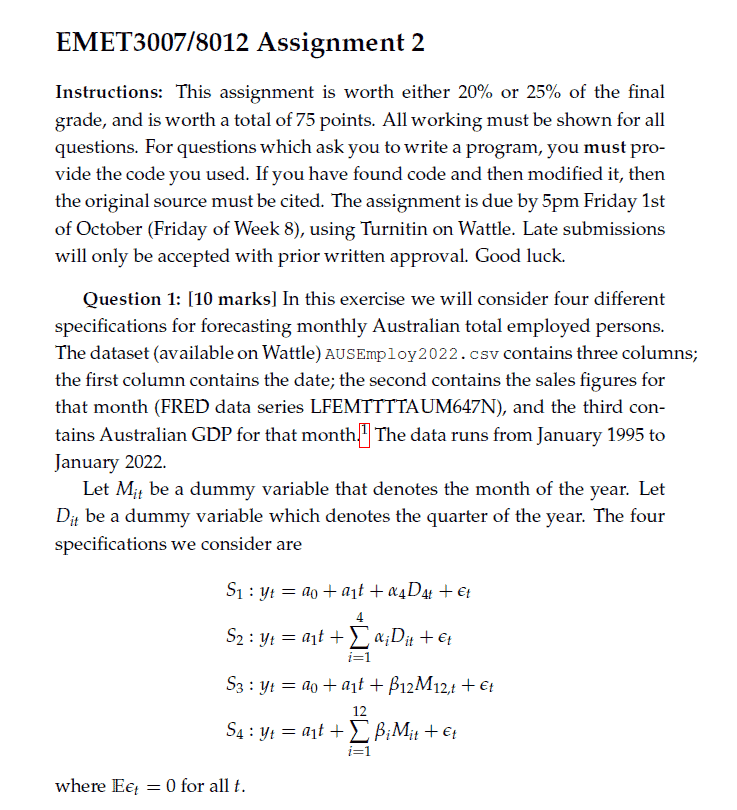

Instructions:

This assignment is worth either 20% or 25% of the final grade, and is worth a total of 75 points. All working must be shown for all questions. For questions which ask you to write a program, you must provide the code you used. If you have found code and then modified it, then the original source must be cited. The assignment is due by 5pm Friday 1st of October (Friday of Week 8), using Turnitin on Wattle. Late submissions will only be accepted with prior written approval. Good luck.

[10 marks] In this exercise we will consider four different specifications for forecasting monthly Australian total employed persons. The dataset (available on Wattle) AUSEmp 1oy 2022. csv contains three columns; the first column contains the date; the second contains the sales figures for that month (FRED data series LFEMTTTTAUM647N), and the third contains Australian GDP for that month.1] The data runs from January 1995 to January $2022 .$

Let $M_{i t}$ be a dummy variable that denotes the month of the year. Let $D_{i t}$ be a dummy variable which denotes the quarter of the year. The four specifications we consider are

$$

\begin{aligned}

&S_1: y_t=a_0+a_1 t+\alpha_4 D_{4 t}+\epsilon_t \

&S_2: y_t=a_1 t+\sum_{i=1}^4 \alpha_i D_{i t}+\epsilon_t \

&S_3: y_t=a_0+a_1 t+\beta_{12} M_{12, t}+\epsilon_t \

&S_4: y_t=a_1 t+\sum_{i=1}^{12} \beta_i M_{i t}+\epsilon_t

\end{aligned}

$$

where $\mathbb{E} \epsilon_t=0$ for all $t$.

a) For each specification, describe this specification in words.

b) For each specification, estimate the values of the parameters, and compute the MSE, $\mathrm{AIC}$, and BIC. If you make any changes to the csv file, please describe the changes you make. As always, you must include your code.

c) For each specification, compute the MSFE for the 1-step and 5-step ahead forecasts, with the out-of-sample forecasting exercise beginning at $T_0=50$.

d) For each specification, plot the out-of-sample forecasts and comment on the results.

[10 marks] Now add to Question 1 the additional assumption that $\epsilon_t \sim \mathcal{N}\left(0, \sigma^2\right)$. One estimator ${ }^2$ for $\sigma^2$ is

$$

\hat{\sigma}^2=\frac{1}{T-k} \sum_{t=1}^T\left(y_t-\hat{y}_t\right)^2

$$

where $\hat{y}_t$ is the estimated value of $y_t$ in the model and $k$ is the number of regressors in the specification.

a) For each specification $\left(S_1, \ldots, S_4\right)$, compute $\hat{\sigma}^2$.

b) For each specification, make a $95 \%$ probability forecast for the sales in June $2021 .$

c) For each specification, compute the probability that the total employed persons in June 2022 will be greater than $13.5$ million. According to the FRED series LFEMTTTTAUM647N, what was the actual employment level for that month.

d) Do you think the assumption that $\epsilon_t$ is iid is a reasonable assumption for this data series.

[10 marks] Here we investigate whether adding GDP $\mathrm{Gs}^3$ as a predictor can improve our forecasts. Consider the following modified specifications:

$$

\begin{aligned}

&S_1^{\prime}: y_t=a_0+a_1 t+\alpha_4 D_{4 t}+\gamma x_{t-h}+\epsilon_t \

&S_2^{\prime}: y_t=a_1 t+\sum_{i=1}^4 \alpha_i D_{i t}+\gamma x_{t-h}+\epsilon_t \

&S_3^{\prime}: y_t=a_0+a_1 t+\beta_{12} M_{12, t}+\gamma x_{t-h}+\epsilon_t \

&S_4^{\prime}: y_t=a_1 t+\sum_{i=1}^{12} \beta_i M_{i t}+\gamma x_{t-h}+\epsilon_t

\end{aligned}

$$

where $\mathbb{E} \epsilon_t=0$ for all $t$, and $x_{t-h}$ is GDP at time $t-h$. For each specification, compute the MSFE for the 1-step ahead, and the 5-step ahead forecasts, with the out-of-sample forecasting exercise beginning at $T_0=50$. For each specification, plot the out-of-sample forecasts and comment on the results.

[15 marks] Here we investigate whether Holt-Winters smoothing can improve our forecasts. Use a Holt-Winters smoothing method with seasonality, to produce 1-step ahead and 5-step ahead forecasts and compute the MSFE for these forecasts. You should use smoothing parameters $\alpha=\beta=\gamma=0.3$ and start the out-of-sample forecasting exercise at $T_0=50$. Plot these out-of-sample forecasts and comment on the results.

Additionally, estimate the values for $\alpha, \beta$, and $\gamma$ which minimise the MSFE. Find the MSFE for these parameter vales and compare it to the baseline $\alpha=\beta=\gamma=0.3$.

[5 marks] Questions 1, 3 and 4 each provided alternative models for forecasting Australian Total Employment. Compare the efficacy of these forecasts. Your comparison should include discussions of MSFE, but must also make qualitative observations (typically based on your graphs).

[10 marks] Develop another model, either based on material from class or otherwise, to forecast Australian Total Employment. Your new model should perform better (have a lower MSFE or MAFE) than all models from Questions 1,3, and 4. As part of your response to this question you must provide:

a) a brief written explanation of what your model is doing,

b) a brief statement on why you think your new model will perform better,

c) any relevant equations or mathematics/statistics to describe the model,

d) the code to run the model, and

e) the MSFE and/or MAFE error found by your model, and a brief discussion of how this compares to previous cases.

[15 marks] Consider the ARX(1) model

$$

y_t=\mu+a t+\rho y_{t-1}+\epsilon_t

$$

where the errors follow an $\mathrm{AR}(2)$ process

$$

\epsilon_t=\phi_1 \epsilon_{t-1}+\phi_2 \epsilon_{t-2}+u_t, \quad \mathbf{u} \sim \mathcal{N}\left(0, \sigma^2 I\right)

$$

for $t=1, \ldots, T$ and $e_{-1}=e_0=0$. Suppose $\phi_1, \phi_2$ are known. Find (analytically) the maximum likelihood estimators for $\mu, a, \rho$, and $\sigma^2$.

Hint: First write $y$ and $\epsilon$ in vector/matrix form. You may wish to use different looking forms for each. Find the distribution of $\epsilon$ and $y$. Then apply some appropriate calculus. You may want to let $H=I-\phi_1 L-\phi_2 L^2$, where $I$ is the $T \times T$ identity matrix, and $L$ is the lag matrix.

时间序列代写

统计代写|时间序列代写Time Series代考 请认准UprivateTA™. UprivateTA™为您的留学生涯保驾护航。

微观经济学代写

微观经济学是主流经济学的一个分支,研究个人和企业在做出有关稀缺资源分配的决策时的行为以及这些个人和企业之间的相互作用。my-assignmentexpert™ 为您的留学生涯保驾护航 在数学Mathematics作业代写方面已经树立了自己的口碑, 保证靠谱, 高质且原创的数学Mathematics代写服务。我们的专家在图论代写Graph Theory代写方面经验极为丰富,各种图论代写Graph Theory相关的作业也就用不着 说。

线性代数代写

线性代数是数学的一个分支,涉及线性方程,如:线性图,如:以及它们在向量空间和通过矩阵的表示。线性代数是几乎所有数学领域的核心。

博弈论代写

现代博弈论始于约翰-冯-诺伊曼(John von Neumann)提出的两人零和博弈中的混合策略均衡的观点及其证明。冯-诺依曼的原始证明使用了关于连续映射到紧凑凸集的布劳威尔定点定理,这成为博弈论和数学经济学的标准方法。在他的论文之后,1944年,他与奥斯卡-莫根斯特恩(Oskar Morgenstern)共同撰写了《游戏和经济行为理论》一书,该书考虑了几个参与者的合作游戏。这本书的第二版提供了预期效用的公理理论,使数理统计学家和经济学家能够处理不确定性下的决策。

微积分代写

微积分,最初被称为无穷小微积分或 “无穷小的微积分”,是对连续变化的数学研究,就像几何学是对形状的研究,而代数是对算术运算的概括研究一样。

它有两个主要分支,微分和积分;微分涉及瞬时变化率和曲线的斜率,而积分涉及数量的累积,以及曲线下或曲线之间的面积。这两个分支通过微积分的基本定理相互联系,它们利用了无限序列和无限级数收敛到一个明确定义的极限的基本概念 。

计量经济学代写

什么是计量经济学?

计量经济学是统计学和数学模型的定量应用,使用数据来发展理论或测试经济学中的现有假设,并根据历史数据预测未来趋势。它对现实世界的数据进行统计试验,然后将结果与被测试的理论进行比较和对比。

根据你是对测试现有理论感兴趣,还是对利用现有数据在这些观察的基础上提出新的假设感兴趣,计量经济学可以细分为两大类:理论和应用。那些经常从事这种实践的人通常被称为计量经济学家。

Matlab代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。