如果你也在 怎样代写会计accounting这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。会计accounting是对经济实体,如企业和公司的财务和非财务信息的衡量、处理和交流。会计被称为 “商业语言”,衡量一个组织的经济活动的结果,并将这些信息传达给各种利益相关者,包括投资者、债权人、管理层和监管者。术语 “会计 “和 “财务报告 “经常被当作同义词使用。

会计accounting可以分为几个领域,包括财务会计、管理会计、税务会计和成本会计。财务会计侧重于向信息的外部用户,如投资者、监管者和供应商报告组织的财务信息,包括编制财务报表;而管理会计侧重于测量、分析和报告信息,供管理层内部使用。记录财务交易,以便在财务报告中提出财务摘要,被称为簿记,其中复式簿记是最常见的系统。 会计信息系统旨在支持会计功能和相关活动。

my-assignmentexpert™ 会计accounting作业代写,免费提交作业要求, 满意后付款,成绩80\%以下全额退款,安全省心无顾虑。专业硕 博写手团队,所有订单可靠准时,保证 100% 原创。my-assignmentexpert™, 最高质量的会计accounting作业代写,服务覆盖北美、欧洲、澳洲等 国家。 在代写价格方面,考虑到同学们的经济条件,在保障代写质量的前提下,我们为客户提供最合理的价格。 由于统计Statistics作业种类很多,同时其中的大部分作业在字数上都没有具体要求,因此会计accounting作业代写的价格不固定。通常在经济学专家查看完作业要求之后会给出报价。作业难度和截止日期对价格也有很大的影响。

想知道您作业确定的价格吗? 免费下单以相关学科的专家能了解具体的要求之后在1-3个小时就提出价格。专家的 报价比上列的价格能便宜好几倍。

my-assignmentexpert™ 为您的留学生涯保驾护航 在会计accounting作业代写方面已经树立了自己的口碑, 保证靠谱, 高质且原创的会计accounting代写服务。我们的专家在会计accounting代写方面经验极为丰富,各种会计accounting相关的作业也就用不着 说。

我们提供的会计accounting及其相关学科的代写,服务范围广, 其中包括但不限于:

会计代写|会计作业代写accounting代考|Introduction

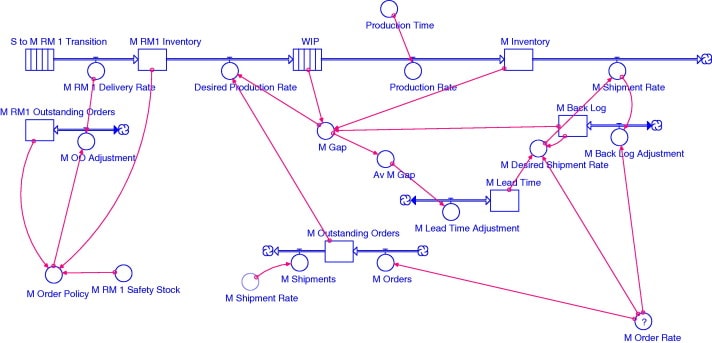

In the preceding chapter, we discussed a variety of methods for collecting data about inventory. The next question one might ask is: What information do I need to collect, and how might this vary depending on the manufacturing system in use? This chapter covers the flow of information through a bare-bones manufacturing system using minimal transactions, one organized under a manufacturing resources planning (MRP II) system, as well as one under a just-in-time system. The differences in transactions required for the various systems, as you will see, are significant.

会计代写|会计作业代写accounting代考|The Simplified Manufacturing System

An entrepreneur decides to manufacture a new product and does so out of his garage until expanded sales allow him to move into a small production facility and hire a few staff to assist in the process. In this home-grown environment, the first required inventory transaction occurs when the fledgling company receives billings from its suppliers subsequent to having ordered supplies, requiring it to record a liability to the supplier and an offsetting inventory asset for whatever was bought. When the company eventually sells products, it must record another transaction to relieve the inventory account for the amount sold, with an offsetting increase in a cost of goods sold account. The basic transactions are noted in Exhibit 2-1 at the points in the cost of goods sold cycle where they occur.

Although this approach is admirable for its spare style, it is severely lacking from both a control and costing standpoint. First, the entrepreneur has no idea if there is any scrap in the manufacturing process, because the system does not relieve any scrap from the system. Second, the purchasing department staff can order inventory whenever they want and in any quantities without anyone knowing if they are doing a good job, because the system has no way of determining how much inventory is actually in stock. Third, the inventory accountant cannot assign production costs to inventory, because there is no device for tracking the status of inventory through production; instead, all production costs must be charged to expense in the current period, even if the company is deliberately building its inventory stocks, resulting in probable losses in the current period and disproportionately high profits when the inventory is later sold. Consequently, the bare-bones style requires little accounting but has a severe impact on one’s ability to run the business.

会计代写|会计作业代写ACCOUNTING代考|A Description of the MRP II System

The MRP II system was a gradual development of computer systems that were designed to bring the advantages of computerization to the manual manufacturing systems in existence before the $1960 \mathrm{~s}$. It began with the creation of databases that tracked inventory. This information had historically been tracked with manually updated index cards or some similar device and was highly prone to error. By shifting to a computer system, companies could make this information available to the purchasing department, where it could be readily consulted when determining how many additional parts to purchase. In addition, the data could now be easily sorted and sifted to see which items were being used the most (and least), which yielded valuable information about what inventory should be kept in stock and what discarded.

The purchasing staff now had better information about the amount of inventory on hand, but they did not know what quantities of materials were going to be used without going through a series of painfully tedious manual calculations. To alleviate this problem, the MRP II system progressed another step by incorporating a production schedule and a bill of materials for every item listed on it. This was an immense step forward, because now the computer system could multiply the units listed on the production schedule by the component parts for each item, as listed on the bills of material, and arrive at the quantities that had to be purchased in order to meet production requirements. This total amount of purchases was then netted against the available inventory to see if anything in stock could be used, before placing orders for more materials. The lead times for the purchase of each part was also incorporated into the computer system, so that it could determine for the purchasing staff the exact dates on which orders for parts must be placed. This new level of automation was called material requirements planning (MRP), because (as the name implies) it revealed the exact quantities and types of materials needed to run a production operation.

会计作业代写

会计代写|会计作业代写ACCOUNTING代考|INTRODUCTION

在前一章中,我们讨论了收集库存数据的各种方法。人们可能会问的下一个问题是:我需要收集哪些信息?这取决于所使用的制造系统如何变化?本章介绍了通过使用最少事务的基本制造系统的信息流,该系统在制造资源计划下组织米R磷一世一世系统,以及即时系统下的系统。正如您将看到的,各种系统所需的事务差异很大。

会计代写|会计作业代写ACCOUNTING代考|THE SIMPLIFIED MANUFACTURING SYSTEM

一位企业家决定制造一种新产品,并在他的车库外这样做,直到扩大销售允许他搬入一个小型生产设施并雇用一些员工来协助该过程。在这种本土环境中,第一个必需的库存交易发生在刚起步的公司在订购供应品后收到供应商的账单时,要求它记录对供应商的负债以及所购买的任何物品的抵销库存资产。当公司最终销售产品时,它必须记录另一笔交易以减少库存账户的销售额,并抵消销货成本账户的增加。图表 2-1 中记录了基本交易发生在商品销售成本周期中的各个点。

尽管这种方法因其备用样式而令人钦佩,但从控制和成本计算的角度来看,它都严重缺乏。首先,企业家不知道制造过程中是否有任何废料,因为系统不会从系统中释放任何废料。其次,采购部门的员工可以随时订购任何数量的库存,而无需任何人知道他们是否做得很好,因为系统无法确定实际库存的数量。第三,库存会计无法将生产成本分配到库存,因为没有通过生产跟踪库存状态的装置;相反,所有生产成本都必须在当期计入费用,即使公司故意增加库存,导致当期很可能发生亏损,而在以后出售存货时可能会产生不成比例的高额利润。因此,准系统风格几乎不需要会计,但会对一个人的经营能力产生严重影响。

会计代写|会计作业代写ACCOUNTING代考|A DESCRIPTION OF THE MRP II SYSTEM

MRP II 系统是计算机系统的逐步发展,旨在将计算机化的优势带入在 2019 年之前存在的手工制造系统中。1960 s. 它始于创建跟踪库存的数据库。历史上,这些信息是通过手动更新的索引卡或一些类似设备进行跟踪的,并且很容易出错。通过转向计算机系统,公司可以将这些信息提供给采购部门,在确定要购买多少额外零件时,可以很容易地查阅这些信息。此外,现在可以轻松地对数据进行分类和筛选,以查看哪些项目被使用得最多一种ndl和一种s吨,这产生了关于哪些库存应该保留以及哪些被丢弃的有价值的信息。

采购人员现在对手头的库存数量有了更好的了解,但他们不知道要使用多少材料,而无需经过一系列痛苦繁琐的手动计算。为了缓解这个问题,MRP II 系统又向前迈进了一步,为其中列出的每个项目合并了生产计划和材料清单。这是向前迈出的一大步,因为现在计算机系统可以将生产计划中列出的单位乘以材料清单上列出的每个项目的组件,并得出必须购买的数量,以便满足生产要求。然后,在订购更多材料之前,将购买的总金额与可用库存相抵消,看看是否可以使用库存中的任何东西。每个零件的采购提前期也被纳入计算机系统,以便它可以为采购人员确定必须下订单的确切日期。这种新的自动化水平被称为物料需求计划米R磷, 因为一种s吨H和n一种米和一世米pl一世和s它揭示了进行生产操作所需的确切材料数量和类型。

会计代写|会计作业代写accounting代考 请认准UprivateTA™. UprivateTA™为您的留学生涯保驾护航。