如果你也在 怎样代写会计accounting这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。会计accounting是对经济实体,如企业和公司的财务和非财务信息的衡量、处理和交流。会计被称为 “商业语言”,衡量一个组织的经济活动的结果,并将这些信息传达给各种利益相关者,包括投资者、债权人、管理层和监管者。术语 “会计 “和 “财务报告 “经常被当作同义词使用。

会计accounting可以分为几个领域,包括财务会计、管理会计、税务会计和成本会计。财务会计侧重于向信息的外部用户,如投资者、监管者和供应商报告组织的财务信息,包括编制财务报表;而管理会计侧重于测量、分析和报告信息,供管理层内部使用。记录财务交易,以便在财务报告中提出财务摘要,被称为簿记,其中复式簿记是最常见的系统。 会计信息系统旨在支持会计功能和相关活动。

my-assignmentexpert™ 会计accounting作业代写,免费提交作业要求, 满意后付款,成绩80\%以下全额退款,安全省心无顾虑。专业硕 博写手团队,所有订单可靠准时,保证 100% 原创。my-assignmentexpert™, 最高质量的会计accounting作业代写,服务覆盖北美、欧洲、澳洲等 国家。 在代写价格方面,考虑到同学们的经济条件,在保障代写质量的前提下,我们为客户提供最合理的价格。 由于统计Statistics作业种类很多,同时其中的大部分作业在字数上都没有具体要求,因此会计accounting作业代写的价格不固定。通常在经济学专家查看完作业要求之后会给出报价。作业难度和截止日期对价格也有很大的影响。

想知道您作业确定的价格吗? 免费下单以相关学科的专家能了解具体的要求之后在1-3个小时就提出价格。专家的 报价比上列的价格能便宜好几倍。

my-assignmentexpert™ 为您的留学生涯保驾护航 在会计accounting作业代写方面已经树立了自己的口碑, 保证靠谱, 高质且原创的会计accounting代写服务。我们的专家在会计accounting代写方面经验极为丰富,各种会计accounting相关的作业也就用不着 说。

我们提供的会计accounting及其相关学科的代写,服务范围广, 其中包括但不限于:

会计代写|会计作业代写accounting代考|What Is an Inventory Control System?

When dealing with inventory, one should be concerned about three issues: (1) the physical quantity of goods in stock and (2) the cost at which they are valued, as well as (3) the proper billing of shipped goods. An inventory control system should be based on these issues. First, its design should minimize the risk that inventory will be lost through any number of means (e.g., pilferage, scrap losses, natural disasters). This does not mean that a vast array of controls should be installed that make it impossible to lose inventory, but at the price of burdening the materials management process with a multitude of non-value-added activities. On the contrary, one must customize the control system so that sufficient controls are in place to mitigate the greatest risks of inventory loss, while avoiding those controls that have comparatively little impact on inventory losses.

Second, the control system should ensure that costs are fairly and consistently applied to inventories. These controls can cover a wide array of areas, such as automation of transaction data entry to avoid entry errors, locking down access to the unit of measure field in the item master file, and controlling the contents of the overhead cost accumulation pools. Many of these controls do not require additional labor to maintain once they are set up, so there can be considerably more controls over inventory costs than may be the case over quantities.

Third, it should ensure that goods shipped are appropriately billed to customers. An inventory control system is less concerned with billing the correct amount to customers; instead, the main point is to ensure that the billing transaction is appropriately triggered by a shipment action.

All of these issues are affected by the accuracy of inventory-related transactions, which are dealt with in the final section of this chapter. The following sections describe many possible controls over various aspects of inventory quantities and controls. They are intended to be a pool of possibilities from which one can make selections, rather than a mandatory array of control requirements.

会计代写|会计作业代写accounting代考|Inventory in Transit

Inventory in transit is an area that is customarily ignored by control system designers, because they tend to think only in terms of on-site inventory. However, this can be a major problem area if the terms of inbound or outbound shipment specify that the company retains ownership of the goods either before or after its arrival at or departure from the company premises. Thus, the key control issues include identification of the ownership of any in-transit inventories, mitigation of ownership risk, and inclusion of owned in-transit items in inventory valuations. The following controls address these issues:

- Ownership: Record intercompany inventory transfers in a central inventory database. If a company shifts inventory from one subsidiary to another, it is possible that the inventory will not be properly relieved from the shipping entity or added by the receiving entity, either of which can cause unit record error. In addition, the receiving entity may record the inventory at a different cost than the shipping entity. Both problems can be resolved by recording inventory transfers in a central inventory database that is used by both subsidiaries. However, these central databases are expensive to purchase and maintain, and also require reliable online access by multiple locations.

- Ownership: Audit both sides of all intercompany transfer transactions. As just noted, both sides of an intercompany inventory transfer can incorrectly record the transaction, resulting in incorrect consolidated financial results. One way to detect these issues after the fact is to regularly schedule an internal audit review of both the shipping and receiving transactions associated with a sample of intercompany transfers. These reviews should result in recommendations to alter the recording system to eliminate errors.

- Ownership: Require a customer signature on every bill-and-hold document. If a company builds products but does not ship them, it can still claim revenue under the assumption that customers have authorized the company to store the units on their behalf. This approach can lead to significant abuse of revenue recognition, so a good control is to require all customers to sign a billand-hold transaction approval document. This document states that customers have authorized the off-site storage and accept ownership of the goods.

- Ownership: Audit shipment terms. Certain types of shipment terms will require that a company shipping goods must retain inventory on its books for some period after the goods have physically left the company, or that a receiving company record inventory on its books before its arrival at the receiving dock. Although in practice most companies will record inventory only when it is physically present, this is technically incorrect under certain shipment terms. Consequently, a company should perform a periodic audit of shipment terms used to see if any deliveries require different inventory treatment.

会计代写|会计作业代写ACCOUNTING代考|Inventory Stocking

Many of the problems associated with inventory originate with the initial decisions to set safety stock levels, add product options, and design new components into products. Although these decisions fall outside of the traditional control systems for inventory, they play a key role in the amount of a company’s inventory investment, and so are included here. All controls noted relate to the addition of stock to inventory.

- Additions: Reject all purchases that are not preapproved. A major flaw in the purchasing systems of many companies is that all supplier deliveries are accepted at the receiving dock, irrespective of the presence of authorizing paperwork. Many of these deliveries are verbally authorized orders from employees throughout the company, many of whom are not authorized to make such purchases. This problem can be eliminated by enforcing a rule that all items received must have a corresponding purchase order on file that has been authorized by the purchasing department. By doing so, the purchasing staff can verify that there is a need for each item requisitioned and that it is bought at a reasonable price from a certified supplier.

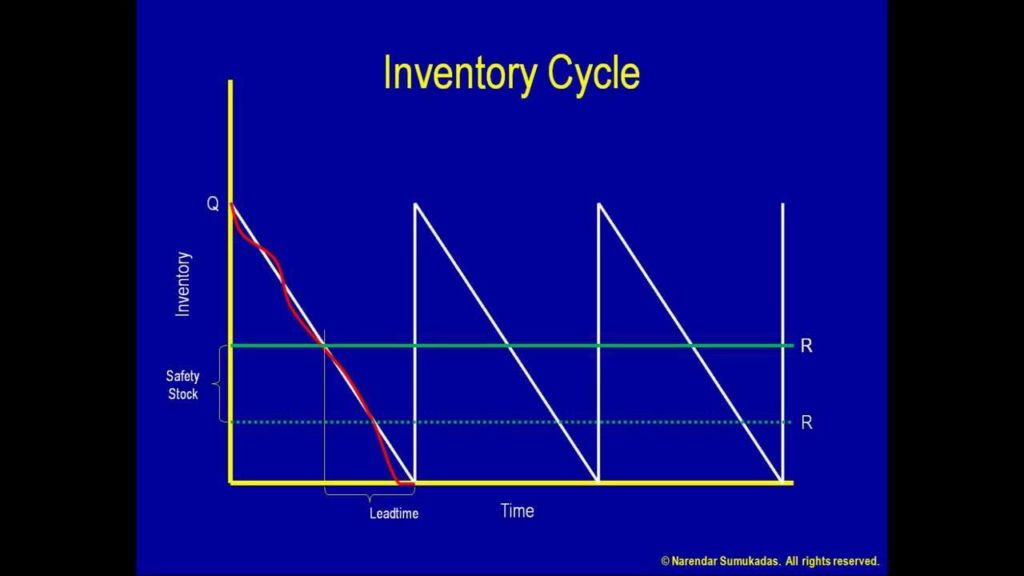

- Additions: Revise safety stock levels for seasonal items. The most common approach to setting safety stock levels is to run a historical usage analysis over the past few years and use that information to decide on an average safety stock level. However, this approach ignores sudden drops in demand caused by seasonality, leaving too much inventory on hand. If demand permanently drops thereafter, safety stock levels will be too high and may represent a risk of obsolescence. A potential control is to mandate quarterly adjustments to safety stock levels of seasonal items, thereby more closely matching supply to demand.

- Additions: Reduce the number of products and product options. Each incremental product that a company chooses to sell requires the storage of more parts. This is a particular problem if there are many variations on the basic product, mandating storage of each product version. To control the number of these inventory additions, schedule a periodic product profitability review and cancel unprofitable products; the determination of unprofitability should certainly include an analysis of the amount of working capital tied up in inventory that is uniquely associated with a particular product.

- Additions: Standardize parts. When engineers design new products, they may not consider using existing components. The result is a plethora of similar but separately tracked components, each of which requires some investment in onhand inventory. An excellent control over these unwanted inventory additions is to require a parts standardization review as an integral step in the development of any new product. To reinforce the concept, consider including the minimization of the total number of on-hand component parts in the bonus plan of the engineering manager.

- Additions: Coordinate engineering change orders with on-hand balances. When the engineering staff implements a change order, new parts are added to a product while the replaced items are no longer needed and remain in stock for prolonged periods. In an environment where engineering change orders are common, a nearly mandatory control is to verify the remaining on-hand balance of any components being rendered obsolete, so that the change orders can be implemented in conjunction with the maximum depletion of existing stocks.

会计作业代写

会计代写|会计作业代写ACCOUNTING代考|WHAT IS AN INVENTORY CONTROL SYSTEM?

在处理库存时,应该关注三个问题:(1)库存货物的实际数量和(2)它们的估价成本,以及(3)发货货物的正确计费。库存控制系统应该基于这些问题。首先,其设计应尽量减少因多种方式(如盗窃、废品损失、自然灾害)造成的库存损失风险。这并不意味着应该安装大量的控制措施来避免库存损失,而是以大量非增值活动为材料管理流程带来负担。相反,必须定制控制系统,以便有足够的控制措施来减轻库存损失的最大风险,

其次,控制系统应确保成本公平一致地应用于存货。这些控制可以涵盖广泛的领域,例如交易数据输入的自动化以避免输入错误,锁定对项目主文件中计量单位字段的访问,以及控制间接费用累积池的内容。许多这些控制一旦建立就不需要额外的劳动力来维护,因此对库存成本的控制可能比对数量的控制要多得多。

第三,应确保向客户收取适当的发货货款。库存控制系统不太关心向客户收取正确的金额;相反,重点是确保计费交易由装运操作适当地触发。

所有这些问题都受到库存相关交易准确性的影响,本章最后一节将讨论这些问题。以下部分描述了对库存数量和控制的各个方面的许多可能的控制。它们旨在成为人们可以从中做出选择的可能性池,而不是一系列强制性的控制要求。

会计代写|会计作业代写ACCOUNTING代考|INVENTORY IN TRANSIT

运输中的库存是控制系统设计人员通常忽略的一个领域,因为他们往往只考虑现场库存。但是,如果入站或出站运输条款规定公司在货物到达或离开公司场所之前或之后保留货物的所有权,则这可能是一个主要问题领域。因此,关键控制问题包括识别任何在途存货的所有权、降低所有权风险以及将拥有的在途物品纳入存货估值。以下控件解决了这些问题:

- 所有权:在中央库存数据库中记录公司间库存转移。如果一家公司将库存从一家子公司转移到另一家子公司,则库存可能无法从运输实体适当地释放或由接收实体添加,这两种情况都可能导致单位记录错误。此外,接收实体可能以不同于运输实体的成本记录库存。这两个问题都可以通过在两个子公司都使用的中央库存数据库中记录库存转移来解决。然而,这些中央数据库的购买和维护成本很高,并且还需要多个位置的可靠在线访问。

- 所有权:审计所有公司间转让交易的双方。如前所述,公司间库存转移的双方都可能错误地记录交易,从而导致合并财务结果不正确。事后发现这些问题的一种方法是定期安排对与公司间转移样本相关的运输和接收交易的内部审计审查。这些审查应导致建议更改记录系统以消除错误。

- 所有权:要求客户在每个开票并持有文件上签名。如果一家公司制造产品但不发货,它仍然可以在假设客户已授权公司代表他们存储这些产品的情况下申请收入。这种方法可能会导致收入确认的严重滥用,因此一个好的控制是要求所有客户签署一张票据持有交易批准文件。该文件表明客户已授权异地存储并接受货物的所有权。

- 所有权:审核装运条款。某些类型的装运条款将要求运输货物的公司必须在货物实际离开公司后的一段时间内将库存保留在其账簿上,或者要求收货公司在其到达收货码头之前在其账簿上记录库存。尽管实际上大多数公司只会在库存实际存在时才记录库存,但在某些装运条款下这在技术上是不正确的。因此,公司应该对用于查看是否有任何交付需要不同的库存处理的装运条款进行定期审核。

会计代写|会计作业代写ACCOUNTING代考|INVENTORY STOCKING

与库存相关的许多问题都源于设定安全库存水平、添加产品选项以及在产品中设计新组件的初始决策。尽管这些决策不属于传统的库存控制系统,但它们在公司的库存投资量中起着关键作用,因此包括在此处。所有提到的控制都与库存增加有关。

- 添加:拒绝所有未经预先批准的购买。许多公司采购系统的一个主要缺陷是,无论是否有授权文件,所有供应商的货物都在收货码头接受。其中许多交付是来自整个公司员工的口头授权订单,其中许多人无权进行此类采购。这个问题可以通过强制执行一条规则来消除,即所有收到的物品必须有一个已由采购部门授权的相应采购订单存档。通过这样做,采购人员可以验证是否需要每个被征用的物品,并且它是从经过认证的供应商那里以合理的价格购买的。

- 补充:修改季节性物品的安全库存水平。设置安全库存水平的最常见方法是对过去几年的历史使用情况进行分析,并使用该信息来确定平均安全库存水平。但是,这种方法忽略了季节性导致的需求突然下降,从而使手头的库存过多。如果此后需求持续下降,安全库存水平将过高,并可能代表过时的风险。一个潜在的控制措施是要求对季节性物品的安全库存水平进行季度调整,从而更紧密地匹配供需。

- 增加:减少产品和产品选项的数量。公司选择销售的每个增量产品都需要存储更多零件。如果基本产品有很多变体,要求存储每个产品版本,这将是一个特殊的问题。为了控制这些库存增加的数量,安排定期的产品盈利能力审查并取消不盈利的产品;确定无利可图当然应该包括分析与特定产品唯一相关的库存中的营运资金数额。

- 补充:标准化零件。当工程师设计新产品时,他们可能不会考虑使用现有的组件。结果是大量类似但单独跟踪的组件,每个组件都需要对现有库存进行一些投资。对这些不必要的库存增加的一个很好的控制是要求零件标准化审查作为任何新产品开发的一个组成部分。为了强化这个概念,考虑在工程经理的奖金计划中包括最小化现有零部件的总数。

- 增加:协调工程变更单与现有余额。当工程人员实施变更单时,新部件被添加到产品中,而被替换的部件不再需要并长期保留在库存中。在工程变更单很常见的环境中,几乎强制性的控制是验证任何被淘汰的组件的剩余现有余额,以便可以在最大程度地消耗现有库存的同时实施变更单。

会计代写|会计作业代写accounting代考 请认准UprivateTA™. UprivateTA™为您的留学生涯保驾护航。