如果你也在 怎样代写金融会计Financial Accounting ACCT1101这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。金融会计Financial Accounting是会计的一个具体分支,涉及记录、总结和报告一段时期内企业经营所产生的无数交易的过程。这些交易被总结为财务报表的编制,包括资产负债表、损益表和现金流量表,这些报表记录了公司在特定时期的经营业绩。

金融会计Financial Accounting是与企业相关的财务交易的总结、分析和报告有关的会计领域。这涉及到编制供公众使用的财务报表。股东、供应商、银行、雇员、政府机构、企业主和其他利益相关者都是有兴趣收到这些信息用于决策的例子。

金融会计Financial Accounting代写,免费提交作业要求, 满意后付款,成绩80\%以下全额退款,安全省心无顾虑。专业硕 博写手团队,所有订单可靠准时,保证 100% 原创。最高质量的金融会计Financial Accounting作业代写,服务覆盖北美、欧洲、澳洲等 国家。 在代写价格方面,考虑到同学们的经济条件,在保障代写质量的前提下,我们为客户提供最合理的价格。 由于作业种类很多,同时其中的大部分作业在字数上都没有具体要求,因此金融会计Financial Accounting作业代写的价格不固定。通常在专家查看完作业要求之后会给出报价。作业难度和截止日期对价格也有很大的影响。

同学们在留学期间,都对各式各样的作业考试很是头疼,如果你无从下手,不如考虑my-assignmentexpert™!

my-assignmentexpert™提供最专业的一站式服务:Essay代写,Dissertation代写,Assignment代写,Paper代写,Proposal代写,Proposal代写,Literature Review代写,Online Course,Exam代考等等。my-assignmentexpert™专注为留学生提供Essay代写服务,拥有各个专业的博硕教师团队帮您代写,免费修改及辅导,保证成果完成的效率和质量。同时有多家检测平台帐号,包括Turnitin高级账户,检测论文不会留痕,写好后检测修改,放心可靠,经得起任何考验!

想知道您作业确定的价格吗? 免费下单以相关学科的专家能了解具体的要求之后在1-3个小时就提出价格。专家的 报价比上列的价格能便宜好几倍。

会计代写|金融会计代考Financial Accounting代写|Gearing and its implications

The relationship between equity and long-term borrowings is known as the gearing (or leverage) of the financial structure. There are two common ways of calculating a gearing ratio:

(a) compare the debt (i.e. long-term borrowings) with the equity; or

(b) compare the debt with the capital employed (i.e. equity plus debt).

Formulae for the two gearing ratios are:

(a) Gearing $=\frac{\text { Debt }}{\text { Share capital }+\text { Reserves }}=\frac{\text { Debt }}{\text { Equity }}$

(b) Gearing $=\frac{\text { Debt }}{\text { Share capital }+\text { Reserves }+\text { Debt }}=\frac{\text { Debt }}{\text { Equity }+\text { Debt }}$

For Bread Co. the figures are:

(a) 20X1: $0.0$ per cent

$20 \times 2: \frac{20}{106}=18.6$ per cent

(b) 20X1: $0.0$ per cent

$$

20 \times 2: \frac{20}{126}=15.9 \text { per cent }

$$

For this company, the shareholders might want to maximise the proportion of the total capital employed that is financed by debt rather than by themselves, as now explained. As shown in Table 7.3, with non-current debt of 20 (measured in $€ 000$ ), the ROCE for Bread Co. for $20 \mathrm{X} 2$ was $19.0$ per cent and the ROE was $20.8$ per cent.

If we were to increase the gearing ratio so that, for example, the same capital employed of 126 consisted instead of capital plus reserves of 66 and debentures (with 10 per cent interest) increased to 60 , then the ratios for $20 \mathrm{X} 2$ would give the same ROCE but a much improved return to the equity investors, as follows:

$$

\operatorname{ROE}=\left(\frac{24-6}{126-60}\right)=\frac{18}{66}=27.3 \text { per cent }

$$

There are limits to the feasibility of increasing the proportion of debt, however. First, it is riskier to lend to a business that already has significant debt and therefore increased interest rates would be needed to attract such lending – if, indeed, it could be attracted at all. Second, consider what happens to a highly geared structure when operating profits fall. Suppose that Bread Co. alters its capital structure (as above) to give owners’ equity of 66 and debentures of 60 , but then in $20 \times 3$ the level of operating profit falls back to that of $20 \mathrm{X} 1$, i.e. 12 . This would lead to $20 \mathrm{X} 3$ ratios as follows:

ROE for $20 \mathrm{X} 3=\left(\frac{12-6}{66}\right)=9.1$ per cent

ROE for $20 \mathrm{X} 3=\left(\frac{12}{126}\right)=9.5$ per cent

Now the gearing is working in the other direction, to magnify the fall in returns suffered by the shareholders rather than to magnify the rise. The end result is that ROE is less than ROCE. It is, of course, perfectly possible for ROCE to be positive and ROE to be negative. It should be remembered also that a company which cannot afford to pay dividends does not have to pay them. However, a company that cannot afford to pay interest still legally has to pay it. This can be the road to bankruptcy.

会计代写|金融会计代考Financial Accounting代写|Further analysis of ROE and ROCE

In practice, business is much more complicated than for Bread Co. The text and case studies in this book are not designed to cover all possible complications that might be met, but to enable the diligent reader to work out how to deal with them. To begin this process, two complications are mentioned at this stage.

What is long-term borrowing?

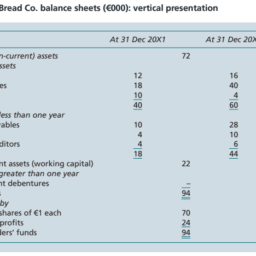

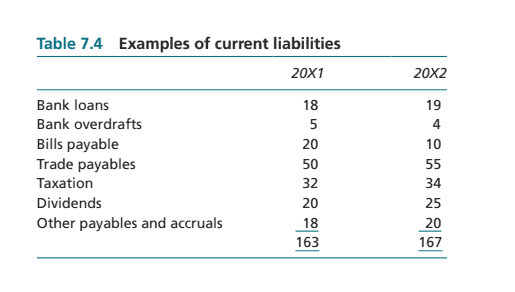

If a particular liability is defined as one of those ‘falling due within one year’ or some similar phrase, the reality behind this may not be clear-cut. For example, consider the amounts set out in Table $7.4$ as falling due within one year.

Does it look as though all of these items are genuine short-term liabilities arising from the trading and operating cycle or do some of them seem to be a continuing source of finance that happens to be legally constructed so as to be renewable within one year? It seems likely that the bank loans and overdrafts, and possibly also the commercial bills payable, are being used to finance the activities of the business, rather than being an integral part of those operating activities.

If that view is taken, then these items might be included as long-term borrowings for the purposes of calculating capital employed. Further, the interest on those ‘current’ liabilities must then also be added back to net profit (or not deducted from operating profit) in arriving at the correct return figure for the ROCE ratio. This may involve a very careful analysis and division of the interest payable amount between the various loans to which it relates. However, care is needed here. We are only discussing the treatment for gearing calculations. If risk of liquidity problems were being discussed (see Section 7.5), some of these financing items might definitely be ‘current’.

金融会计代考

会计代奇金融会计代考FINANCIAL ACCOUNTING代 Э|GEARING AND ITS IMPLICATIONS

股权和长期借款之间的关系被称为资产负债率 orleverage的财务结构。有两种常用的计算资产负债率的方法:

$a$ 比较债务i.e.long-termborrowings用股权;或者

$b$ 比较债务与使用的资本i.e. equityplusdebt.

两个资产负债率的公式为:

$a$ 传动装置 $=\frac{\text { Debt }}{\text { Share capital + Reserves }}=\frac{\text { Debt }}{\text { Equity }}$

$b$ 传动装置 $=\frac{\text { Debt }}{\text { Share capital + Reserves + Debt }}=\frac{\text { Debt }}{\text { Equity + Debt }}$

Bread Co. 的数据是:

$a 20 \times 1: 0.0$ 百分

$20 \times 2: \frac{20}{106}=18.6$ 百分

b20x1: $0.0$ 百分

$$

20 \times 2: \frac{20}{126}=15.9 \text { per cent }

$$

对于这家公司,股东可能希望最大限度地利用债务融资而不是目己融资的总资本比例,正如现在所解释的那样。如表 $7.3$ 所示,非流动负债为 20 measuredin $\$ \in 000 \$$ ,面包公司的 ROCE 为 $20 \mathrm{X} 2$ 曾是 $19.0 \%$ ,净资产收益率为 $20.8$ 百分。

如果我们要提高资产负债率,例如,相同的已动用资本为 126 ,而不是资本加准备金 66 和债券with 10percentinterest增加到 60 ,那么比率为 $20 \times 2$ 会给股权投资 者带来相同的 ROCE,但会大大提高回报,如下所示:

$$

\text { ROE }=\left(\frac{24-6}{126-60}\right)=\frac{18}{66}=27.3 \text { per cent }

$$

然而,提高债务比例的可行性是有限度的。首先,向已经背负巨额债务的企业提供佶款风险更大,因此需要提高利率才能吸引此类贷款一一如果确实能够吸引的 话。其次,考虑当苕业利润下降时高杠杆结构会发生什么。假设面包公司改变了它的资本结构asabove给予 66 的所有者权益和 60 的债券,但随后 $20 \times 3$ 菅业利润 水平回落至 $20 \mathrm{X} 1$, 即 12 。这会导致 $20 \mathrm{X} 3$ 比率如下:

净资产收益率为 $20 \mathrm{X} 3=\left(\frac{12-6}{66}\right)=9.1$ 百分比

股本回报率 $20 \mathrm{X} 3=\left(\frac{12}{126}\right)=9.5$ 百分

现在,杠杆率正朝着另一个方向发挥作用,放大股东所遭受的回报下降而不是扩大回报。最终结果是 ROE 小于 ROCE。当然,完全有可能 ROCE 为正而 ROE 为负。 还应记住,无力支付股息的公司不必支付。但是,无力支付利息的公司仍然必须依法支付。这可能是走向破产的道路。

会计代写|金融会计代考FINANCIAL ACCOUNTING代 写|FURTHER ANALYSIS OF ROE AND ROCE

在实践中,业务比面包公司复杂得多。本书中的文字和安例研究并非旨在涵盖所有可能遇到的复杂情况,而是为了让勤奋的读者能够弄清楚如何处理它们。为了开 始这个过程,在这个阶段提到了两个并发症。

什么是长期借款?

如果将特定负债定义为“一年内到期”或类似短语之一,则其背后的现实可能并不明确。例如,考虑表中列出的金额 $7.4$ 一年内到期。

看起来所有这些项目是否都是由交易和运营周期产生的真正的短期负债,或者其中一些似乎是一种持续的资金来源,恰好是合法构建的,可以在一年内更新? 银行 贷款和透支以及可能还有商业应付票据似乎很可能被用于为企业活动提供资金,而不是作为这些经莒活动的组成部分。

如果采用这种观点,那么为了计算已动用咨本,这些项目可能会被列为长期借款。此外,这些“流动”负债的利息也必须加回到净利润中 ornotdeducted fromoperatingprofit得出 ROCE 比率的正确回报数字。这可能涉及对其相关的各种贷款之间的应付利息金额进行非常仔细的分析和划分。但 是,这里需要小心。我们只讨论杠杆计算的处理方法。如果正在讨论流动性问题的风险seeSection $7.5$ ,其中一些融资项目可能绝对是“当前”的。

会计代写|金融会计代考Financial Accounting代写 请认准UprivateTA™. UprivateTA™为您的留学生涯保驾护航。

微观经济学代写

微观经济学是主流经济学的一个分支,研究个人和企业在做出有关稀缺资源分配的决策时的行为以及这些个人和企业之间的相互作用。my-assignmentexpert™ 为您的留学生涯保驾护航 在数学Mathematics作业代写方面已经树立了自己的口碑, 保证靠谱, 高质且原创的数学Mathematics代写服务。我们的专家在图论代写Graph Theory代写方面经验极为丰富,各种图论代写Graph Theory相关的作业也就用不着 说。

线性代数代写

线性代数是数学的一个分支,涉及线性方程,如:线性图,如:以及它们在向量空间和通过矩阵的表示。线性代数是几乎所有数学领域的核心。

博弈论代写

现代博弈论始于约翰-冯-诺伊曼(John von Neumann)提出的两人零和博弈中的混合策略均衡的观点及其证明。冯-诺依曼的原始证明使用了关于连续映射到紧凑凸集的布劳威尔定点定理,这成为博弈论和数学经济学的标准方法。在他的论文之后,1944年,他与奥斯卡-莫根斯特恩(Oskar Morgenstern)共同撰写了《游戏和经济行为理论》一书,该书考虑了几个参与者的合作游戏。这本书的第二版提供了预期效用的公理理论,使数理统计学家和经济学家能够处理不确定性下的决策。

微积分代写

微积分,最初被称为无穷小微积分或 “无穷小的微积分”,是对连续变化的数学研究,就像几何学是对形状的研究,而代数是对算术运算的概括研究一样。

它有两个主要分支,微分和积分;微分涉及瞬时变化率和曲线的斜率,而积分涉及数量的累积,以及曲线下或曲线之间的面积。这两个分支通过微积分的基本定理相互联系,它们利用了无限序列和无限级数收敛到一个明确定义的极限的基本概念 。

计量经济学代写

什么是计量经济学?

计量经济学是统计学和数学模型的定量应用,使用数据来发展理论或测试经济学中的现有假设,并根据历史数据预测未来趋势。它对现实世界的数据进行统计试验,然后将结果与被测试的理论进行比较和对比。

根据你是对测试现有理论感兴趣,还是对利用现有数据在这些观察的基础上提出新的假设感兴趣,计量经济学可以细分为两大类:理论和应用。那些经常从事这种实践的人通常被称为计量经济学家。

Matlab代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。