如果你也在 怎样代写宏观经济学Macroeconomics ECON2022这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。宏观经济学Macroeconomics对国家或地区经济整体行为的研究。它关注的是对整个经济事件的理解,如商品和服务的生产总量、失业水平和价格的一般行为。宏观经济学关注的是经济体的表现–经济产出、通货膨胀、利率和外汇兑换率以及国际收支的变化。减贫、社会公平和可持续增长只有在健全的货币和财政政策下才能实现。

宏观经济学Macroeconomics(来自希腊语前缀makro-,意思是 “大 “+经济学)是经济学的一个分支,处理整个经济体的表现、结构、行为和决策。例如,使用利率、税收和政府支出来调节经济的增长和稳定。这包括区域、国家和全球经济。根据经济学家Emi Nakamura和Jón Steinsson在2018年的评估,经济 “关于不同宏观经济政策的后果的证据仍然非常不完善,并受到严重批评。宏观经济学家研究的主题包括GDP(国内生产总值)、失业(包括失业率)、国民收入、价格指数、产出、消费、通货膨胀、储蓄、投资、能源、国际贸易和国际金融。

同学们在留学期间,都对各式各样的作业考试很是头疼,如果你无从下手,不如考虑my-assignmentexpert™!

my-assignmentexpert™提供最专业的一站式服务:Essay代写,Dissertation代写,Assignment代写,Paper代写,Proposal代写,Proposal代写,Literature Review代写,Online Course,Exam代考等等。my-assignmentexpert™专注为留学生提供Essay代写服务,拥有各个专业的博硕教师团队帮您代写,免费修改及辅导,保证成果完成的效率和质量。同时有多家检测平台帐号,包括Turnitin高级账户,检测论文不会留痕,写好后检测修改,放心可靠,经得起任何考验!

经济代写|宏观经济学代考Macroeconomics代写|Assets and Liabilities of a Bank

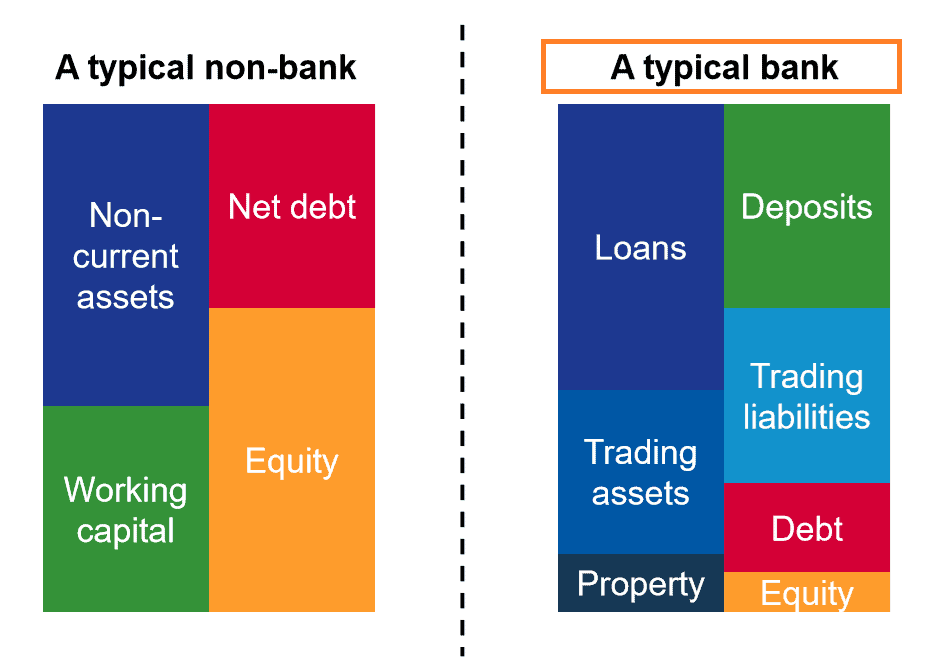

Banks are businesses, and like all enterprises they incur liabilities and accumulate assets. The confusing thing about banks is that by accepting a deposit, which is after all an inflow of money to the institution, the bank has incurred a liability. Since a liability is an obligation to pay, the bank has, by accepting the deposit, promised to pay the depositor the amount of his deposit plus accumulated interest either on demand or at a particular time. In the same way, by making a loan, which is an outflow of money from the bank, the bank has accumulated an asset. An asset is a claim to payment, and by making the loan, the bank has a claim on some repayment schedule of principal plus interest. Not all loans are repaid, so the bank must estimate the expected value of loans that will not be repaid and count this against its assets. Thus bank balance sheets have an item marked “Outstanding Loans net of Loss Reserve”. This loss reserve is a polite term for the expected value of loan defaults.

A bank also holds, by law, a certain proportion of its deposits in zero-interest accounts with the Federal reserve system. These are also assets, although pretty low-yield ones. Banks hold a very small amount of “vault cash” which is currency (notes and coins) held at the bank (usually in impressive safes). This is used to meet the cash needs of depositors dayto-day. Banks also directly hold securities like U.S. Government debt (bonds). The nature of these securities is limited by law, so in the U.S. banks are not big stock market players. Banks also often directly own property, such as the bank building itself.

Like other business, banks make operating profits or losses as the value of assets and liabilities fluctuate. If a bank makes a profit, so that assets exceed liabilities, a residual liability is added to balance assets and adjusted liabilities. Thus profit is a liability. The opposite is true for losses. ${ }^1$

In this chapter we are going to assume that banks are zero cost enterprises with no assets other than loans and no liabilities other than deposits. We will assume that banks make zero economic profit in expectation, so the expected return on loans must cover the amount owed to depositors.

经济代写|宏观经济学代考Macroeconomics代写|Fractional Reserve Banking and the Money Supply

In the U.S. today, banks are required to hold a certain fraction of their deposits in reserve, that is, not lend them out (these reserves are held on deposit by the retail banks at Federal Reserve member banks). Since the reserve requirement is not $100 \%$, banks may lend out the portion of their deposits not held on reserve. Reserve requirements are indexed by the nature of deposits and loans, so banks have to hold extra reserves against riskier loans, but let us suppose for a moment that they are constant at $10 \%$. Imagine that the government prints $\$ 100$ and gives it to household 0 , so $H_0=100$. This household immediately places it in the bank or spends it. Any amount spent must go as a payment to some other household, which then faces the same choice: deposit or spending. And so on, until the banking system has absorbed the entire $\$ 100$ of cash.

In this way, the fractional reserve banking system can multiply an infusion of cash, augmenting the M1 money supply by more than the infusion. Reserves held at the Fed will also affect the money supply in the same way. For this reason, cash and reserves held at the Fed are often called base money or high-powered money. The sum of all cash and deposits held at the Fed is called the monetary base.

Assume for simplicity that each household simply deposits the cash. Assume also that there is only one common bank. Now since the reserve requirement is $10 \%$, the bank places $\$ 10$ of its new deposits on reserve at the local Federal Reserve system member bank. The remaining $\$ 90$ it lends out again to some other household, household 1 , so $H_1=90$. This household spends or deposits the money, as before, so a further $\$ 90$ of deposits appear in the bank. Now the bank sends $\$ 9$ to the Federal Reserve, and lends out $\$ 81$ to household 2 , so $\mathrm{H}2=81$. This process continues until the bank is lending out, to household $i$ an amount $H_i$ $$ H_i=\$ 100(1-0.10)^i $$ The amount of new money created is just the sum of all loans made to households as a result of the original $\$ 100$ transfer, plus that $\$ 100$. That is: $$ M^{\prime}-M=\sum{i=0}^{\infty} H_i=\sum_{i=0}^{\infty} 100(1-0.10)^i=100 \sum_{i=0}^{\infty} 0.90^i=100 \frac{1}{1-0.90}=1000 .

$$

宏观经济学代写

经济代写|宏观经济学代考MACROECONOMICS代 写|ASSETS AND LIABILITIES OF A BANK

银行是企业,与所有企业一样,它们承担负债并积㽧资产。银行令人困惑的是,通过接受存款,这毕竟是资金流入该机构,银行承担了责任。由 于负债是一种支付义务,银行通过接受存款,承诺向存款人支付其存款金额加上傫积利息,或者在要求时或在特定时间。同样,通过发放贷款 (即资金从银行流出),银行积㽧了资产。资产是一种付款请求权,通过提供贷款,银行对某些本金加利息的还款计划拥有请求权。并非所有贷 款都得到偿还,因此银行必须估计不会偿还的贷款的预期价值,并将其计入其资产。因此,银行资产负债表中有一个项目标有“扣除损失准备金后 的末偿还贷款”。这种损失准备金是对贷款违约预期价值的礼貌用语。

根据法律,银行还持有一定比例的存款在联邦储备系统的零利率账户中。这些也是资产,尽管收益很低。银行持有极少量的“金库现金”,即货币 notesandcoins在银行举行usuallyinimpressivesafes. 这用于满足储户日常的现金需求。银行还直接持有美国政府债券等证券bonds. 这些证 券的性质受法律限制,因此在美国银行不是大型股票市场参与者。银行通常也直接拥有财产,例如银行大楼本身。

与其他业务一样,银行会随着资产和负债价值的波动而产生营业利润或亏损。如果银行盈利,资产超过负债,剩余负债将添加到资产余额和调整 后的负债中。因此,利润是一种负债。损失则相反。 1

在本章中,我们将假设银行是零成本企业,除贷款外没有其他资产,除存款外没有其他负债。我们假设银行的预期经济利润为零,因此贷款的预 期回报率必须覆盖对存款人的欠款。

经济代写|宏观经济学代考MACROECONOMICS代 写|FRACTIONAL RESERVE BANKING AND THE MONEY SUPPLY

在今天的美国,银行必须持有一定比例的存款作为准备金,即不得借出

thesereservesareheldondepositbytheretailbanksatFederalReservememberbanks. 由于准备金要求不 $100 \%$, 银行可以借出末作为准备金 持有的部分存款。准备金要求与存款和贷款的性质挂钩,因此银行必须为风险较高的贷款持有额外的准备金,但让我们暂时假设它们保持不变 $10 \%$. 想象一下,政府印刷 $\$ 100$ 并将它交给家庭 0,所以 $H_0=100$. 这个家庭立即将其存入银行或花掉。任何花费的金额都必须支付给其他一些家 庭,然后这些家庭将面临相同的选择:存款或支出。依此类推,直到银行系统吸收了整个 $\$ 100$ 现金。

通过这种方式,部分准备金银行系统可以增加现金注入,增加 $M 1$ 货币供应量超过注入量。美联储持有的储备金也会以同样的方式影响货币供应 量。因此,美联储持有的现金和准备金通常被称为基础货币或高能货币。美联储持有的所有现金和存款的总和称为基础货币。

为简单起见,假设每个家庭只存入现金。还假设只有一个公共银行。现在由于准备金要求是 $10 \%$, 银行地方 $\$ 10$ 其在当地联邦储备系统成员银行的 新存款准备金。其余 $\$ 90$ 它再次借给其他家庭,家庭 1 ,所以 $H_1=90$. 这个家庭像以前一样花钱或存钱,所以进一步 $\$ 90$ 存款出现在银行。现在银 行发 $\$ 9$ 给美联储,并借出 $\$ 81$ 到家庭 2 ,所以 $\mathrm{H} 2=81$. 这个过程一直持续到银行贷款给家庭擞量 $H_i$

$$

H_i=\$ 100(1-0.10)^i

$$

创造的新货币数量恰好是由于原始货币而向家庭发放的所有贷款的总和 $\$ 100$ 转移,再加上 $\$ 100$. 那是:

$$

M^{\prime}-M=\sum i=0^{\infty} H_i=\sum_{i=0}^{\infty} 100(1-0.10)^i=100 \sum_{i=0}^{\infty} 0.90^i=100 \frac{1}{1-0.90}=1000 .

$$

经济代写|宏观经济学代考Macroeconomics代写 请认准exambang™. exambang™为您的留学生涯保驾护航。

微观经济学代写

微观经济学是主流经济学的一个分支,研究个人和企业在做出有关稀缺资源分配的决策时的行为以及这些个人和企业之间的相互作用。my-assignmentexpert™ 为您的留学生涯保驾护航 在数学Mathematics作业代写方面已经树立了自己的口碑, 保证靠谱, 高质且原创的数学Mathematics代写服务。我们的专家在图论代写Graph Theory代写方面经验极为丰富,各种图论代写Graph Theory相关的作业也就用不着 说。

线性代数代写

线性代数是数学的一个分支,涉及线性方程,如:线性图,如:以及它们在向量空间和通过矩阵的表示。线性代数是几乎所有数学领域的核心。

博弈论代写

现代博弈论始于约翰-冯-诺伊曼(John von Neumann)提出的两人零和博弈中的混合策略均衡的观点及其证明。冯-诺依曼的原始证明使用了关于连续映射到紧凑凸集的布劳威尔定点定理,这成为博弈论和数学经济学的标准方法。在他的论文之后,1944年,他与奥斯卡-莫根斯特恩(Oskar Morgenstern)共同撰写了《游戏和经济行为理论》一书,该书考虑了几个参与者的合作游戏。这本书的第二版提供了预期效用的公理理论,使数理统计学家和经济学家能够处理不确定性下的决策。

微积分代写

微积分,最初被称为无穷小微积分或 “无穷小的微积分”,是对连续变化的数学研究,就像几何学是对形状的研究,而代数是对算术运算的概括研究一样。

它有两个主要分支,微分和积分;微分涉及瞬时变化率和曲线的斜率,而积分涉及数量的累积,以及曲线下或曲线之间的面积。这两个分支通过微积分的基本定理相互联系,它们利用了无限序列和无限级数收敛到一个明确定义的极限的基本概念 。

计量经济学代写

什么是计量经济学?

计量经济学是统计学和数学模型的定量应用,使用数据来发展理论或测试经济学中的现有假设,并根据历史数据预测未来趋势。它对现实世界的数据进行统计试验,然后将结果与被测试的理论进行比较和对比。

根据你是对测试现有理论感兴趣,还是对利用现有数据在这些观察的基础上提出新的假设感兴趣,计量经济学可以细分为两大类:理论和应用。那些经常从事这种实践的人通常被称为计量经济学家。

Matlab代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。