如果你也在 怎样统计计算Statistical Computing这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。统计计算Statistical Computing是统计学和计算机科学之间的纽带。它意味着通过使用计算方法来实现的统计方法。它是统计学的数学科学所特有的计算科学(或科学计算)的领域。这一领域也在迅速发展,导致人们呼吁应将更广泛的计算概念作为普通统计教育的一部分。与传统统计学一样,其目标是将原始数据转化为知识,[2]但重点在于计算机密集型统计方法,例如具有非常大的样本量和非同质数据集的情况。

许多统计建模和数据分析技术可能难以掌握和应用,因此往往需要使用计算机软件来帮助实施大型数据集并获得有用的结果。S-Plus是公认的最强大和最灵活的统计软件包之一,它使用户能够应用许多统计方法,从简单的回归到时间序列或多变量分析。该文本广泛涵盖了许多基本的和更高级的统计方法,集中于图形检查,并具有逐步说明的特点,以帮助非统计学家充分理解方法。

my-assignmentexpert™统计计算Statistical Computing作业代写,免费提交作业要求, 满意后付款,成绩80\%以下全额退款,安全省心无顾虑。专业硕 博写手团队,所有订单可靠准时,保证 100% 原创。my-assignmentexpert™, 最高质量的统计计算Statistical Computing作业代写,服务覆盖北美、欧洲、澳洲等 国家。 在代写价格方面,考虑到同学们的经济条件,在保障代写质量的前提下,我们为客户提供最合理的价格。 由于统计Statistics作业种类很多,同时其中的大部分作业在字数上都没有具体要求,因此统计计算Statistical Computing作业代写的价格不固定。通常在经济学专家查看完作业要求之后会给出报价。作业难度和截止日期对价格也有很大的影响。

想知道您作业确定的价格吗? 免费下单以相关学科的专家能了解具体的要求之后在1-3个小时就提出价格。专家的 报价比上列的价格能便宜好几倍。

my-assignmentexpert™ 为您的留学生涯保驾护航 在统计计算Statistical Computing作业代写方面已经树立了自己的口碑, 保证靠谱, 高质且原创的统计计算Statistical Computing代写服务。我们的专家在统计计算Statistical Computing代写方面经验极为丰富,各种统计计算Statistical Computing相关的作业也就用不着 说。

我们提供的统计计算Statistical Computing及其相关学科的代写,服务范围广, 其中包括但不限于:

- 随机微积分 Stochastic calculus

- 随机分析 Stochastic analysis

- 随机控制理论 Stochastic control theory

- 微观经济学 Microeconomics

- 数量经济学 Quantitative Economics

- 宏观经济学 Macroeconomics

- 经济统计学 Economic Statistics

- 经济学理论 Economic Theory

- 计量经济学 Econometrics

统计代写

数学代写|统计计算作业代写Statistical Computing代考|Properties

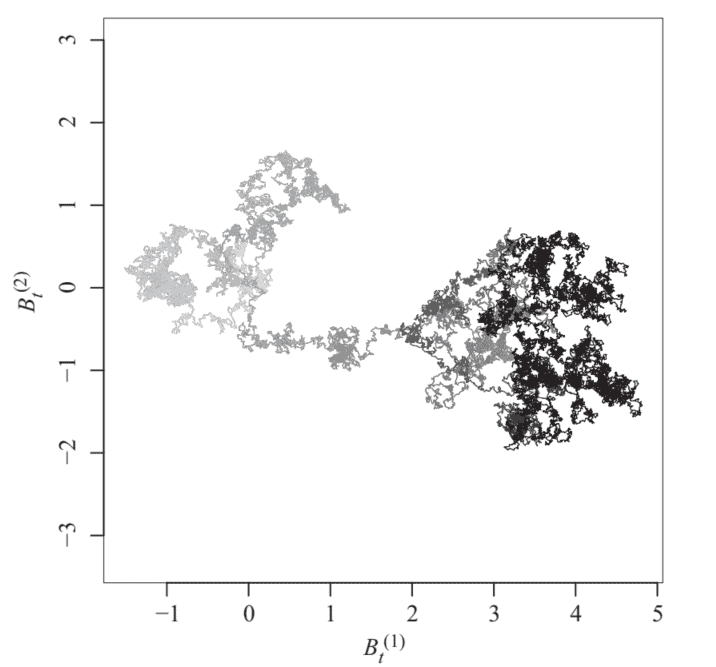

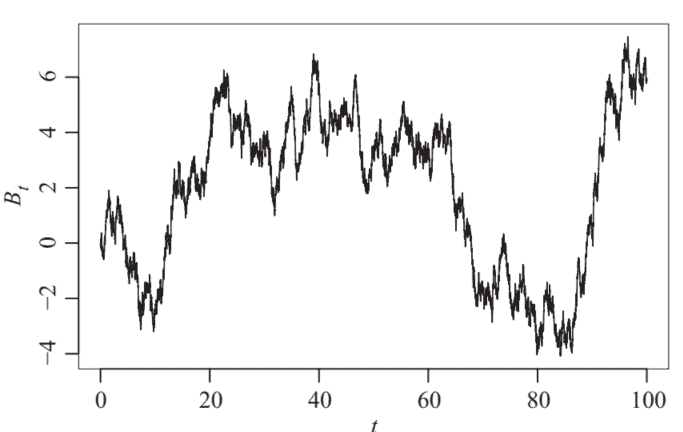

In this section we briefly state some of the most important properties of Brownian motion. Using definition $6.1$, we can immediately derive the following results:

- We have $B_{t}=B_{t}-B_{0} \sim \mathcal{N}\left(0, t I_{d}\right)$ and in particular the expectation of $B_{t}$ is $\mathbb{E}\left(B_{t}\right)=0 .$

- For the one-dimensional case we find $B_{t} \sim \mathcal{N}(0, t)$ and thus the standard deviation of $B_{t}$ is $\sqrt{t}$.

- Similarly, for any dimension, we find that $B_{t}$ has the same distribution as $\sqrt{t} B_{1}$. Thus, the magnitude of $\left|B_{t}\right|$ only grows like $\sqrt{t}$ as $t$ increases.

Another basic result, relating the one-dimensional case to the $d$-dimensional case, is given in the following lemma.

数学代写|统计计算作业代写STATISTICAL COMPUTING代考|Direct simulation

As we have seen at the start of this chapter, we cannot hope to simulate all of the infinitely many values $\left(B_{t}\right){t \geq 0}$ on a computer simultaneously. Instead, we restrict ourselves to simulating the values of $B$ for times $0=t{0}<t_{1}<\cdots<t_{n}$. For a Brownian motion, this can be easily done by using the first two conditions from definition $6.1$ : we have $B_{0}=0$ and $B_{t_{i}}$ can be computed from $B_{t_{i-1}}$ by adding an $\mathcal{N}\left(0, t_{i}-t_{i-1}\right)$ distributed random value, independent of all values computed so far. This method is described in the following algorithm.

input:

sample times $0=t_{0}<t_{1}<\cdots<t_{n}$

randomness used:

an i.i.d. sequence $\left(\varepsilon_{i}\right){i=1,2, \ldots, n}$ with distribution $\mathcal{N}(0,1)$ output: a sample of $B{t_{0}}, \ldots, B_{t_{n}}$, that is a discretised path of a Brownian motion

1: $B_{0} \leftarrow 0$

2: for $i=1,2, \ldots, n$ do

3: $\quad$ generate $\varepsilon_{i} \sim \mathcal{N}(0,1)$

4: $\quad \Delta B_{i} \leftarrow \sqrt{t_{i}-t_{i-1}} \varepsilon_{i}$

5: $\quad B_{t_{i}} \leftarrow B_{t_{i-1}}+\Delta B_{i}$

$6:$ end for

7: return $\left(B_{t_{i}}\right)_{i=0,1, \ldots, n}$

数学代写|统计计算作业代写STATISTICAL COMPUTING代考|Interpolation and Brownian bridges

If we have already simulated values of a Brownian motion $B$ for a set of times, it is possible to refine the simulated path afterwards by simulating values of $B$ for additional times. This method is called interpolation of the Brownian path. Since these additional simulations need to be compatible with the already sampled values, some care is needed when implementing this method.

Assume that we know the values of $B$ at times $0=t_{0}<t_{1}<\cdots<t_{n}$ and that we want to simulate an additional value for $B$ at time $s$ with $t_{i-1}<s<t_{i}$ for some $i \in{2,3, \ldots, n}$. As an abbreviation we write $r=t_{i-1}$ and $t=t_{i}$. By the Markov property of Brownian motion (lemma 6.5, part (b)), the increment $B_{s}-B_{r}$ is independent of $\left(B_{u}\right){0 \leq u \leq r}$. Similarly, $\left(B{u}-B_{t}\right){u \geq t}$ is independent of $\left(B{u}\right){0 \leq u \leq t}$ and thus of $B{s}-B_{r}$. Consequently, we only need to take the value $B_{t}=B_{t_{i}}$ into account when sampling the increment $B_{s}-B_{r}$; by independence the remaining $B_{t_{j}}$ with $j \neq i$ do not affect the distribution of $B_{s}-B_{r}$.

数学代写|统计计算作业代写STATISTICAL COMPUTING代考|PROPERTIES

在本节中,我们简要说明布朗运动的一些最重要的性质。使用定义6.1,我们可以立即得出以下结果:

- 我们有乙吨=乙吨−乙0∼ñ(0,吨一世d)尤其是期望乙吨是和(乙吨)=0.

- 对于一维情况,我们发现乙吨∼ñ(0,吨)因此标准差乙吨是吨.

- 同样,对于任何维度,我们发现乙吨具有相同的分布吨乙1. 因此,幅度|乙吨|只会长得像吨作为吨增加。

另一个基本结果,将一维情况与d维情况,在以下引理中给出。

数学代写|统计计算作业代写STATISTICAL COMPUTING代考|DIRECT SIMULATION

正如我们在本章开头所看到的,我们不能希望模拟所有无限多的值 $\left(B_{t}\right){t \geq 0}$ on a computer simultaneously. Instead, we restrict ourselves to simulating the values of $B$ for times $0=t{0}<t_{1}<\cdots<t_{n}$. For a Brownian motion, this can be easily done by using the first two conditions from definition $6.1$ : we have $B_{0}=0$ and $B_{t_{i}}$ can be computed from $B_{t_{i-1}}$ by adding an $\mathcal{N}\left(0, t_{i}-t_{i-1}\right)$ 分布式随机值,独立于目前计算的所有值。该方法在以下算法中描述。

输入:

采样时间0=吨0<吨1<⋯<吨n

使用的随机性:

input:

sample times $0=t_{0}<t_{1}<\cdots<t_{n}$ randomness used:

an i.i.d. sequence $\left(\varepsilon_{i}\right){i=1,2, \ldots, n}$ with distribution $\mathcal{N}(0,1)$ output: a sample of $B{t_{0}}, \ldots, B_{t_{n}}$, that is a discretised path of a Brownian motion

1: $B_{0} \leftarrow 0$

2: for $i=1,2, \ldots, n$ do

3: generate $\varepsilon_{i} \sim \mathcal{N}(0,1)$

$\begin{array}{ll}\text { 4: } & \Delta B_{i} \leftarrow \sqrt{t_{i}-t_{i-1}} \varepsilon_{i} \ 5: & B_{t_{i}} \leftarrow B_{t_{i-1}}+\Delta B_{i}\end{array}$

6: end for

7: return $\left(B_{t_{i}}\right)_{i=0,1, \ldots, n}$

数学代写|统计计算作业代写STATISTICAL COMPUTING代考|INTERPOLATION AND BROWNIAN BRIDGES

如果我们已经模拟了布朗运动的值乙在一段时间内,可以通过模拟以下值来改进模拟路径乙额外的时间。这种方法称为布朗路径的插值。由于这些额外的模拟需要与已经采样的值兼容,因此在实施此方法时需要小心。

假设我们知道乙有时0=吨0<吨1<⋯<吨n并且我们想要模拟一个附加值乙有时s和吨一世−1<s<吨一世对于一些一世∈2,3,…,n. 作为缩写,我们写r=吨一世−1和吨=吨一世. 由布朗运动的马尔可夫性质一世和米米一种6.5,p一种r吨(b),增量乙s−乙r独立于 $B$ at time $s$ with $t_{i-1}<s<t_{i}$ for some $i \in{2,3, \ldots, n}$. As an abbreviation we write $r=t_{i-1}$ and $t=t_{i}$. By theMarkov property of Brownian motion (lemma 6.5, part (b)), the increment $B_{s}-B_{r}$ is independent of $\left(B_{u}\right){0 \leq u \leq r}$. Similarly, $\left(B{u}-B_{t}\right){u \geq t}$ is independent of $\left(B{u}\right){0 \leq u \leq t}$ and thus of $B{s}-B_{r}$. Consequently, we only need to take the value $B_{t}=B_{t_{i}}$ into account when sampling the increment $B_{s}-B_{r}$; by independence the remaining $B_{t_{j}}$ with $j \neq i$ do not affect the distribution of $B_{s}-B_{r}$.

Assume that $B$ is one-dimensional with $B_{r}=a$. Since $\left(B_{u+r}-B_{r}\right){u \geq 0}$ is a Brownian motion independent of $B{r}$, we have $B_{s} \sim \mathcal{N}(a, s-r)$ and $B_{t}-B_{s} \sim$ $\mathcal{N}(0, t-s)$, independently of each other. Thus, the joint density of $\left(B_{s}, B_{t}\right)$ is

。

计量经济学代写请认准my-assignmentexpert™ Economics 经济学作业代写

微观经济学代写请认准my-assignmentexpert™ Economics 经济学作业代写

宏观经济学代写请认准my-assignmentexpert™ Economics 经济学作业代写