如果你也在 怎样代写风险投资及私募股权Venture Capital and Private Equity ENT4424这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。风险投资及私募股权Venture Capital and Private Equity从技术上讲,风险投资(VC)是私募股权的一种形式。主要区别在于,私募股权投资者更喜欢稳定的公司,而风险投资人通常在创业阶段进入。风险投资通常给予具有惊人增长潜力的小公司。

风险投资及私募股权Venture Capital and Private Equity是私募股权融资的一种形式,由风险投资公司或基金提供给被认为具有高增长潜力的初创企业、早期企业和新兴企业,或者已经显示出高增长(在员工人数、年收入、经营规模等方面)的企业。风险投资公司或基金对这些早期阶段的公司进行投资,以换取股权,或所有权股份。风险资本家承担着为有风险的初创企业融资的风险,希望他们支持的一些公司能够获得成功。由于初创企业面临高度的不确定性,风险投资的失败率很高。初创企业通常基于一种创新的技术或商业模式,它们通常来自高科技行业,如信息技术(IT)、清洁技术或生物技术。

风险投资及私募股权Venture Capital and Private Equity代写,免费提交作业要求, 满意后付款,成绩80\%以下全额退款,安全省心无顾虑。专业硕 博写手团队,所有订单可靠准时,保证 100% 原创。最高质量的风险投资及私募股权Venture Capital and Private Equity作业代写,服务覆盖北美、欧洲、澳洲等 国家。 在代写价格方面,考虑到同学们的经济条件,在保障代写质量的前提下,我们为客户提供最合理的价格。 由于作业种类很多,同时其中的大部分作业在字数上都没有具体要求,因此风险投资及私募股权Venture Capital and Private Equity作业代写的价格不固定。通常在专家查看完作业要求之后会给出报价。作业难度和截止日期对价格也有很大的影响。

同学们在留学期间,都对各式各样的作业考试很是头疼,如果你无从下手,不如考虑my-assignmentexpert™!

my-assignmentexpert™提供最专业的一站式服务:Essay代写,Dissertation代写,Assignment代写,Paper代写,Proposal代写,Proposal代写,Literature Review代写,Online Course,Exam代考等等。my-assignmentexpert™专注为留学生提供Essay代写服务,拥有各个专业的博硕教师团队帮您代写,免费修改及辅导,保证成果完成的效率和质量。同时有多家检测平台帐号,包括Turnitin高级账户,检测论文不会留痕,写好后检测修改,放心可靠,经得起任何考验!

想知道您作业确定的价格吗? 免费下单以相关学科的专家能了解具体的要求之后在1-3个小时就提出价格。专家的 报价比上列的价格能便宜好几倍。

我们在金融 Finaunce代写方面已经树立了自己的口碑, 保证靠谱, 高质且原创的金融 Finaunce代写服务。我们的专家在风险投资及私募股权Venture Capital and Private Equity代写方面经验极为丰富,各种风险投资及私募股权Venture Capital and Private Equity相关的作业也就用不着说。

金融代写|风险投资及私募股权代写Venture Capital and Private Equity代考|Multitask Moral Hazard

Multitask moral hazard refers to situations that involve multiple tasks that the agent may undertake, and only a subset of these tasks benefit the principal (Holmstrom and Milgrom, 1991). A common example of multitask moral hazard involves the entrepreneur as principal and venture capitalist as agent. The venture capitalist will have more than one investee entrepreneurial firm and thus has multiple tasks as an agent for different entrepreneurial firms. The venture capitalist may spend comparatively more time helping a specific entrepreneurial firm in the portfolio. For instance, if the venture capitalist believes a certain investee entrepreneurial firm is going to be far more profitable than the others, he might spend more time ensuring the success of that entrepreneurial firm and less time with other entrepreneurial firms for which he is an agent.

Another common example of multitask moral hazard involves an institutional investor as principal and the venture capitalist as agent. The institutional investor prefers that the venture capitalist works toward maximizing the expected value of the venture capital fund portfolio of entrepreneurial firms in which it has invested on behalf of the institutional investor. As mentioned in Chapter 1, limited partnership funds typically have a lifespan of 10 years. Venture capital fund managers therefore must allocate some of their time fundraising to start another fund before their current fund is wound up to ensure continuity (and employment). The time spent by the venture capital fund manager fundraising does not help increase the value of the existing portfolio investments. Therefore, institutional investors will typically place contractual limits on venture capital fund manager fundraising activities to ensure that sufficient effort is exerted in the portfolio investments. Issues involving limited partnership contracts are discussed further in Chapter $5 .$

金融代写|风险投资及私募股权代写Venture Capital and Private Equity代考|Adverse Selection

Moral hazard, bilateral moral hazard, and multitask moral hazard all refer to agency problems that may arise after a contract is entered into between a principal and an agent (ex post). An agency problem can also exist even before a contract is signed (ex ante). This agency problem is known as adverse selection. The seminal work on adverse selection by George Ackerlof, Michael Spence, and Joseph Stiglitz led to their joint Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel in 2001 (also known as the Nobel Memorial Prize in Economic Sciences). ${ }^{10}$

At a general level in the context of contracting, adverse selection refers to the problem that offers of different types of contracts attract different types of parties to the contract. This problem is usefully illustrated in the context of offers of nonconvertible debt versus common equity finance. An investor that offers debt finance will attract a different type of entrepreneur than an investor that offers equity finance (DeMeza and Webb, 1987, 1992; Stiglitz and Weiss, 1981). We illustrate this proposition by considering two examples. In the first example, we consider entrepreneurs that differ by their level of risk and not their expected mean return. In the second example, we consider entrepreneurs that differ by their expected return, not by their level of risk.

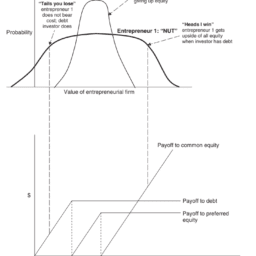

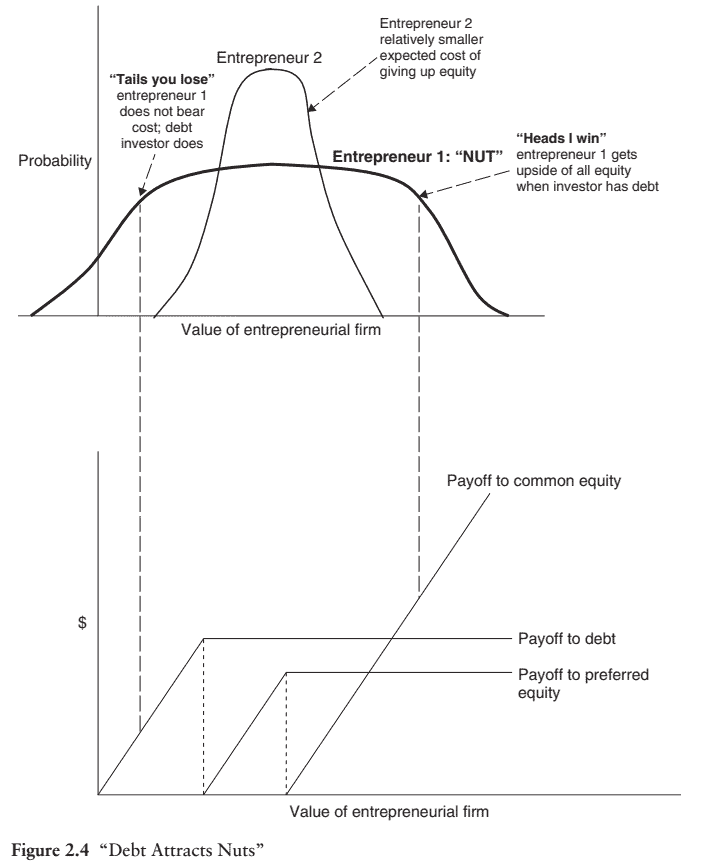

First, let’s consider entrepreneurial firms that have the same expected value but different expected risk. In statistics, we would say that the entrepreneurial firms have the same first moment (expect return) but different second moments (expected risk) of the returns distribution. This situation is illustrated in the top part of Figure 2.4, which presents probability distribution functions (graphs of the expected value of the entrepreneurial firm under different states of nature). In Figure 2.4, Entrepreneur 1 is riskier than Entrepreneur 2 . There is a high probability that Entrepreneur 1 will be very valuable (a “home run”) but also a high probability than Entrepreneur 1 will go bankrupt. Entrepreneur 2, by contrast, has a high probability of a modest value and a low probability of being a home run and a low probability of going bankrupt. Due to the high risk, Entrepreneur 1 is referred to as a “nut” by Stiglitz and Weiss (1981) and other works. In practice, we might think of Entrepreneur 1 as a high-tech generic product that has a stable demand from consumers.

Entrepreneur 1 is more likely to be attracted to offers of nonconvertible debt $^{11}$ financing than by offers of common equity financing. If Entrepreneur 1’s venture turns out to be successful, then Entrepreneur 1 is better off by holding all of the common equity and not sharing common equity with the investor. In Figure 2.4, this is indicated at the point labeled “Heads I win,” which is what Entrepreneur 1 says [to himself in reference to the investor] if the project turns out successfully and the investor has nonconvertible debt. If Entrepreneur $1 \mathrm{had}$ common equity financing, Entrepreneur 1 would have to share the upside of the successful project with the investor and thereby significantly dilute the profits that Entrepreneur 1 would enjoy as an owner. In the payoff diagram below the probability distribution functions in Figure $2.4$, notice the difference between the value of common equity versus nonconvertible debt.

风险投资及私募股权代写

金融代写|风险投资及私募股权代写VENTURE CAPITAL AND PRIVATE EQUITY代考|MULTITASK MORAL HAZARD

多任务道德风险是指涉及代理人可能承担的多项任务的情况,并且这些任务中只有一部分任务对委托人有利HolmstromandMilgrom,1991.多任务道德风险的 一个常见例子是企业家作为委托人,风险资本家作为代理人。风险投资家将拥有不止一个被投资的创业公司,因此作为不同创业公司的代理人有多项任务。风险投 资家可能会花费相对更多的时间来邦助投资组合中的特定创业公司。例如,如果风险投资家相信某家被投资的创业公司将比其他公司盈利得多,他可能会花更多的 时间来确保该创业公司的成功,而不是花更少的时间与他代理的其他创业公司打交道。

多任务道德风险的另一个常见例子涉及作为委托人的机构投资者和作为代理人的风险资本家。机构投资者更喜欢风险投资家致力于最大化其代表机构投资者投资的 创业公司的风险投资基金投资组合的预期价值。如第 1 章所述,有限合伙基金的寿命通常为 10 年。因此,风险投资基金经理必须在当前基金清盘之前分配部分时 间来启动另一只基金,以确保连续性andemployment. 风险投资基金经理等款所花费的时间无助于增加现有投资组合的价值。因此,机构投资者通常会对风险投 资基金经理的筹资活动设置合同限制,以确保在投资组合中付出足够的努力。涉及有限合伙合同的问题将在本章中进一步讨论 5 .

金融代写|风险投资及私募股权代写VENTURE CAPITAL AND PRIVATE EQUITY代考|ADVERSE SELECTION

道德风险、双边道德风险和多任务道德风险都是指委托人和代理人签订合同后可能出现的代理问题expost. 甚至在合同签订之前也可能存在代理问题exante. 这个 代理问题被称为逆向选择。乔治·阿克洛夫、迈克尔·斯宾塞和约瑟夫·斯蒂格利茨在逆向选择方面的开创性工作导致他们在 2001 年联合获得瑞典央行经济科学奖以纪 念阿尔弗雷德·诺贝尔alsoknownastheNobelMemorialPrizeinEconomicSciences. ${ }^{10}$

在合同的一般层面上,逆向选择是指不同类型合同的报价吸引不同类型的合同当事人的问题。这个问题在提供不可转换债务与普通股融资的背景下得到了有用的说 明。提供债务融资的投资者与提供股权融资的投资者将吸引不同类型的企业家 DeMezaandWebb, 1987, 1992; StiglitzandWeiss, 1981. 我们通过考虑两个例子 来说明这个命题。在第一个例子中,我们考虑的企业家的风险水平不同,而不是他们的预期平均回报。在第二个例子中,我们考虑的企业家的不同之处在于他们的 预期回报,而不是他们的风险水平。

首先,让我们考虑具有相同预期价值但不同预期风险的创业公司。在统计学中,我们会说创业公司有相同的第一时刻expectreturn但不同的第二时刻 expectedrisk的回报分布。这种情况在图 $2.4$ 的上半部分进行了说明,它展示了概率分布函数

graphsoftheexpectedvalueoftheentrepreneurialfirmunderdifferentstatesofnature. 在图 $2.4$ 中,企业家 1 比企业家 2 风险百大。企业家 1 很有可能非 常有价值 $a$ “homerun”而且比企业家1破产的概率也高。相比之下,企业家 2 具有中等价值的高概率和本垒打的低概率以及破产的低概率。由于高风险,企业家 1 被 Stiglitz和 Weiss 称为““坚果”1981和其他作品。在实践中,我们可以将 Entrepreneur 1 视为具有稳定消费者需求的高科技通用产品。

企业家 1 更有可能被不可转换债券的报价所吸引 ${ }^{11}$ 融资而不是通过提供普通股融资。如果企业家 1 的企业成功了,那么企业家 1 最好持有所有普通股而不与投资者 分享普通股。在图 $2.4$ 中,这在标记为“Heads I win”的点上表示出来,这就是企业家 1 所说的

tohimsel finrefencetotheinvestor

如果项目成功并且投资者有不可转换的债务。如果创业者1had普通股融资,企业家 1 将不得不与投资者分字成功项目的好处,从而显着稀释企业家 1 作为所有者字 有的利润。在下图的概率分布函数的支付图中 2.4,请注意普通股与不可转换债务的价值之间的差异。

金融代写|风险投资及私募股权代写Venture Capital and Private Equity代考 请认准UprivateTA™. UprivateTA™为您的留学生涯保驾护航。

微观经济学代写

微观经济学是主流经济学的一个分支,研究个人和企业在做出有关稀缺资源分配的决策时的行为以及这些个人和企业之间的相互作用。my-assignmentexpert™ 为您的留学生涯保驾护航 在数学Mathematics作业代写方面已经树立了自己的口碑, 保证靠谱, 高质且原创的数学Mathematics代写服务。我们的专家在图论代写Graph Theory代写方面经验极为丰富,各种图论代写Graph Theory相关的作业也就用不着 说。

线性代数代写

线性代数是数学的一个分支,涉及线性方程,如:线性图,如:以及它们在向量空间和通过矩阵的表示。线性代数是几乎所有数学领域的核心。

博弈论代写

现代博弈论始于约翰-冯-诺伊曼(John von Neumann)提出的两人零和博弈中的混合策略均衡的观点及其证明。冯-诺依曼的原始证明使用了关于连续映射到紧凑凸集的布劳威尔定点定理,这成为博弈论和数学经济学的标准方法。在他的论文之后,1944年,他与奥斯卡-莫根斯特恩(Oskar Morgenstern)共同撰写了《游戏和经济行为理论》一书,该书考虑了几个参与者的合作游戏。这本书的第二版提供了预期效用的公理理论,使数理统计学家和经济学家能够处理不确定性下的决策。

微积分代写

微积分,最初被称为无穷小微积分或 “无穷小的微积分”,是对连续变化的数学研究,就像几何学是对形状的研究,而代数是对算术运算的概括研究一样。

它有两个主要分支,微分和积分;微分涉及瞬时变化率和曲线的斜率,而积分涉及数量的累积,以及曲线下或曲线之间的面积。这两个分支通过微积分的基本定理相互联系,它们利用了无限序列和无限级数收敛到一个明确定义的极限的基本概念 。

计量经济学代写

什么是计量经济学?

计量经济学是统计学和数学模型的定量应用,使用数据来发展理论或测试经济学中的现有假设,并根据历史数据预测未来趋势。它对现实世界的数据进行统计试验,然后将结果与被测试的理论进行比较和对比。

根据你是对测试现有理论感兴趣,还是对利用现有数据在这些观察的基础上提出新的假设感兴趣,计量经济学可以细分为两大类:理论和应用。那些经常从事这种实践的人通常被称为计量经济学家。

Matlab代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。