MY-ASSIGNMENTEXPERT™可以为您提供lse.ac.uk FM302 Corporate Finance公司金融学课程的代写代考和辅导服务!

这是伦敦政经学校公司金融学课程的代写成功案例。

FM302课程简介

This course introduces concepts and theories to critically assess major corporate financial policy decisions. The course focuses in particular on a firm’s capital structure and the impact of taxes, bankruptcy costs, agency conflicts, and asymmetric information on a firm’s financing decisions. We will also discuss other major topics in corporate finance, such as the market for corporate control. In developing tools to analyze these issues, we will introduce the key concepts of corporate finance theory, including debt overhang, risk shifting, and the free-rider problem.

Prerequisites

Formative coursework

Students will be expected to produce 9 problem sets in the LT.

Indicative reading

Detailed course programmes and reading lists are distributed at the start of the course. Illustrative texts include: “Financial Markets and Corporate Strategy” by Hillier, Grinblatt and Titman. “Corporate Finance” by Ivo Welch, and “The Theory of Corporate Finance” by Tirole.

FM302 Corporate Finance HELP(EXAM HELP, ONLINE TUTOR)

When do we use a capital-employed analysis of the balance sheet? And when do we use a solvency-and-liquidity analysis of the balance sheet?

Which approach to the balance sheet should you adopt:

- when giving a warranty on the balance sheet of a company being sold?

- when forecasting a company’s working capital?

Do liabilities that arise during the operating cycle always have a maturity of less than one year?

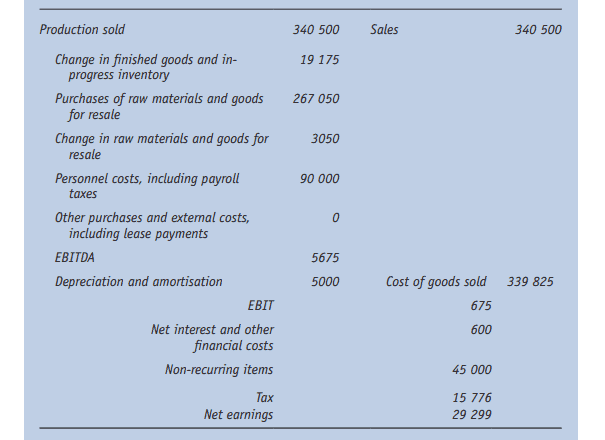

“Classify the following as “stocks”, in/outflows, or change in in/outflows: sales, trade receivables, change in trade receivables, increase in dividends, financial expense, increase in sales, EBITDA.

‘A company’s sales clearly represent a source of funds. However, they do not appear on the balance sheet. Why?

‘Classify the following balance sheet items under fixed assets, working capital, shareholders’ equity or net debt: overdraft, retained earnings, brands, taxes payable, finished goods inventories, bonds.

Capital-employed analysis of the balance sheet: for understanding the company’s use of funds and how they were financed. Solvency-and-liability analysis of the balance sheet: for listing all assets and liabilities.

The solvency-and-liquidity analysis, the capital-employed analysis.

No, in some industries, there is a long period between the invoice date and customer payment (e.g. movie rights).

Inflow, “stocks”, inflow, change in outflow, outflow, change in inflow, inflow.

The balance resulting from the activity is what appears on the balance sheet, i.e. the profit or loss, not the activity itself measured by sales.

In order of listing: net debt, shareholders’ equity, fixed assets, working capital, working capital, net debt.

Is a company that is currently unable to pay its debts always insolvent?

Assess the liquidity of the following assets: plant, unlisted securities, listed securities, head office building located in the centre of a large city, ships and aircraft, commercial paper, raw materials inventories, work-in-progress inventories.

Give a synonym for net assets.

What is another way of describing a difference in “stocks”?

In order of listing: net debt, shareholders’ equity, fixed assets, working capital, working capital, net debt.

In theory, no, as the company may be facing a temporary credit crunch, but most of the time yes because it will have to dispose of assets quickly or stop its activities which will result in a big reduction in equity, and then it is in insolvency.

In order of decreasing liquidity: listed securities, commercial paper, raw materials inventories, head office, unlisted securities, ships and aircraft, work-in-progress inventories, plant.

Shareholders’ equity.

An inflow or outflow.

What is the difference between liabilities and sources of funds?

What is another way of describing a cumulative inflow or outflow?

Give examples of businesses with positive working capital.

‘Give examples of businesses with negative working capital.

The main manufacturers of telephony equipment (Ericsson, Nokia, etc.) provided telecoms operators (Deutsche Telekom, Swisscom, etc.) with substantial supplier credit lines in order to assist them in financing the construction of their UMTS networks. State your views.

/Sources of funds include shareholders’ equity (which does not have to be repaid and is consequently not a liability) and liabilities (which sooner or later have to be repaid). /A “stock”.

Most businesses: publishers, appliance manufacturers, chemical industry, etc.

Movie theatres (no inventories, cash payment from clients), pay TV (subscriptions paid in advance), public works (advance payment from clients).

These are, in fact, merely financial loans and not operating loans, granted to enable the telecoms operator to buy the equipment made by the manufacturer. These loans should be treated as fixed assets on the manufacturer’s balance sheet and as financial debts on the telecom operator’s balance sheet.

MY-ASSIGNMENTEXPERT™可以为您提供LSE.AC.UK FM302 CORPORATE FINANCE公司金融学课程的代写代考和辅导服务!