如果你也在 怎样代写投资组合Portfolio Theory 这个学科遇到相关的难题,请随时右上角联系我们的24/7代写客服。投资组合Portfolio Theory是管理是构建投资组合的持续过程,它平衡了投资者的目标和投资组合经理对未来的期望。这一动态过程为投资者提供了回报。

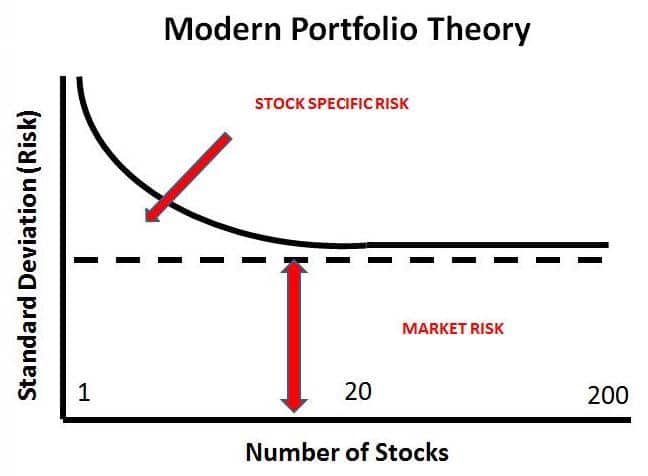

投资组合Portfolio Theory管理中,单个资产或投资是根据其对投资者投资组合的风险和回报的贡献来评估的,而不是孤立地评估。这被称为投资组合视角。在这个过程中,与投资于单个资产或证券相比,通过构建多样化的投资组合,投资组合经理可以在给定的预期回报水平上降低风险。根据现代投资组合理论(MPT),不遵循投资组合观点的投资者承担了没有获得更高预期回报的风险。与2007-2008年金融危机等市场动荡时期相比,投资组合多元化在金融市场正常运行时效果最佳。在动荡时期,相关性往往会增加,从而降低了多样化的好处。相关性是衡量两种证券或市场之间收益变动的标准化指标。

投资组合Portfolio Theory代写,免费提交作业要求, 满意后付款,成绩80\%以下全额退款,安全省心无顾虑。专业硕 博写手团队,所有订单可靠准时,保证 100% 原创。最高质量的投资组合Portfolio Theory作业代写,服务覆盖北美、欧洲、澳洲等 国家。 在代写价格方面,考虑到同学们的经济条件,在保障代写质量的前提下,我们为客户提供最合理的价格。 由于作业种类很多,同时其中的大部分作业在字数上都没有具体要求,因此投资组合Portfolio Theory作业代写的价格不固定。通常在专家查看完作业要求之后会给出报价。作业难度和截止日期对价格也有很大的影响。

同学们在留学期间,都对各式各样的作业考试很是头疼,如果你无从下手,不如考虑my-assignmentexpert™!

my-assignmentexpert™提供最专业的一站式服务:Essay代写,Dissertation代写,Assignment代写,Paper代写,Proposal代写,Proposal代写,Literature Review代写,Online Course,Exam代考等等。my-assignmentexpert™专注为留学生提供Essay代写服务,拥有各个专业的博硕教师团队帮您代写,免费修改及辅导,保证成果完成的效率和质量。同时有多家检测平台帐号,包括Turnitin高级账户,检测论文不会留痕,写好后检测修改,放心可靠,经得起任何考验!

想知道您作业确定的价格吗? 免费下单以相关学科的专家能了解具体的要求之后在1-3个小时就提出价格。专家的 报价比上列的价格能便宜好几倍。

金融代写|投资组合代写Portfolio Theory代考|The Equity Premium Puzzle and Excess Volatility

The equity premium puzzle is an important example of the application of behavioral ideas to explain aggregate stock market movements. Mehra and Prescott (1985) coined the term equity premium puzzle after finding that the neoclassical intertemporal CAPM (ICAPM) was unable to explain the historical premium that equities earned over Treasuries in US financial markets. This puzzle actually constitutes a triplet of puzzles involving the equity premium, the risk-free rate, market volatility, and the predictability of returns and is based on the notion that plausible parameters in the Mehra-Prescott model cannot explain the magnitude of the historical equity premium, return volatility, and return predictability in the US market. Campbell, Lo, and MacKinlay (1996) point out that the neoclassical model implies an equity premium of 0.1 percent, not the historical 3.9 percent; a return standard deviation of 12 percent, not the historical 18 percent; and the absence of predictability in returns, not the predictability observed in practice.

The main behavioral approach to explaining the equity premium involves the work of Benartzi and Thaler (1995) and Barberis, Huang, and Santos (2001). Both approaches feature a representative investor whose preferences are based on prospect theory, which is briefly described in the introduction. While neoclassical expected utility theory emphasizes risk aversion in respect to total consumption or wealth on the part of investors, prospect theory emphasizes loss aversion in respect to changes in consumption or wealth. Behavioral theories of the equity premium puzzle focus on how short investment-time horizons might induce loss-averse investors to behave as if they were extremely averse to risk, thereby inducing a high equity premium in the market. Additionally, if investors are concerned that they have ambiguous beliefs about stock market returns, suggesting that they realize their subjective beliefs might be in error, then they might demand an additional premium to be compensated not just for what they regard as risk but also for the discomfort of knowing that their estimates of risk are imprecise. This additional premium, known as an ambiguity aversion premium, puts additional upward pressure on the equity premium.

金融代写|投资组合代写Portfolio Theory代考|Critiques and Counterarguments

The behavioral perspective continues to evolve along with associated debates. Some of these debates involve behavioral proponents on one side and neoclassical proponents on the other. Other debates feature differing behavioral explanations for particular empirical phenomena. The following sections offer some illustrative examples.

CLOSED-END FUNDS

An early debate about closed-end funds involved Chen, Kan, and Miller (1993) on the neoclassical side and Chopra, Lee, Shleifer, and Thaler (1993) on the behavioral side. Chen, Kan, and Miller suggested that the relationship between fund discounts and small firm returns is neither robust over time nor affected by the degree of institutional ownership. In response, Chopra et al. demonstrated that for 90 percent of small-firm stocks, when discounts narrow, lower institutional ownership stocks do better than higher institutional ownership stocks.

Fama (1998) presents a critique of the literature on over- and underreaction. He points out that instances of overreaction appear about as often as instances of underreaction and suggests that this feature is consistent with market efficiency. According to this view, a market is efficient when price and fundamental value coincide on average, with any deviations due solely to chance. In this respect, the mean abnormal return is zero; however, random fluctuations give rise to nonzero deviations (anomalies) in both directions.

Fama (1998) provides a critical assessment of some of the key articles discussed above, including De Bondt and Thaler (1985); Jegadeesh and Titman (1993); Barberis, Shleifer, and Vishny (1998); and Daniel, Hirshleifer, and Subrahmanyam (1998). Fama’s criticisms vary in nature. He points out that the Fama and French $(1992,1996)$ three-factor risk model can explain the effects reported by both De Bondt and Thaler (1985) and Ikenberry, Lakonishok, and Vermaelen (1995). Hence, he argues that the efficient market paradigm can accommodate these effects. He dismisses both Barberis, Shleifer, and Vishny (1998) and Daniel, Hirshleifer, and Subrahmanyam (1998) for a lack of robustness, asserting that these theories may explain the anomalies they were built to address but fail to explain others sharing similar traits. Fama finds that the studies that pose the most significant challenge to the EMH pertain to postearnings announcement drift (Bernard and Thomas, 1990). The finding concerning postearnings announcement drift is that earnings surprises appear to be positively autocorrelated, suggesting that analysts underreact to earnings announcements. Moreover, there is drift in the associated stock returns, suggesting that investors as a whole underreact. Notably, the drift is short term and is followed by a long-term reversal.

投资组合代写

金融代写|投资组合代写Portfolio Theory代考|The Equity Premium Puzzle and Excess Volatility

股票溢价之谜是应用行为理论解释股票市场总体走势的一个重要例子。Mehra和Prescott(1985)在发现新古典跨期CAPM (ICAPM)无法解释美国金融市场上股票相对于国债的历史溢价后,创造了“股票溢价之谜”一词。这个谜题实际上由三个谜题组成,涉及股票溢价、无风险利率、市场波动性和回报的可预测性,并且基于Mehra-Prescott模型中的合理参数无法解释美国市场历史股票溢价、回报波动性和回报可预测性的大小。Campbell, Lo和MacKinlay(1996)指出,新古典模型暗示股票溢价为0.1%,而不是历史上的3.9%;收益率标准差为12%,而不是历史上的18%;在回报中缺乏可预测性,而不是在实践中观察到的可预测性。

解释股权溢价的主要行为方法涉及Benartzi和Thaler(1995)以及Barberis、Huang和Santos(2001)的工作。这两种方法都有一个代表性的投资者,他们的偏好是基于前景理论的,这在引言中有简要描述。新古典预期效用理论强调投资者在总消费或财富方面的风险规避,而前景理论强调在消费或财富变化方面的损失规避。股票溢价之谜的行为理论关注的是,短期投资时间如何可能导致厌恶损失的投资者表现得好像他们极度厌恶风险,从而导致市场上的高股票溢价。此外,如果投资者担心他们对股票市场回报有模糊的信念,这表明他们意识到自己的主观信念可能是错误的,那么他们可能会要求额外的溢价,不仅要补偿他们认为的风险,还要补偿他们知道自己对风险的估计不精确所带来的不适。这种额外的溢价,被称为模糊性规避溢价,给股票溢价带来了额外的上行压力。

金融代写|投资组合代写Portfolio Theory代考|Critiques and Counterarguments

行为视角随着相关的争论而不断发展。在这些辩论中,行为主义的支持者和新古典主义的支持者站在了一边。其他辩论则以对特定经验现象的不同行为解释为特色。下面几节提供了一些说明性示例。

封闭式基金

关于封闭式基金的早期争论涉及新古典主义方面的Chen、Kan和Miller(1993)和行为方面的Chopra、Lee、Shleifer和Thaler(1993)。Chen, Kan和Miller认为,基金折扣和小企业回报之间的关系既不稳定,也不受机构持股程度的影响。作为回应,Chopra等人证明,对于90%的小公司股票,当折扣收窄时,较低的机构持股股票比较高的机构持股股票表现更好。

Fama(1998)对过度反应和反应不足的文献进行了批判。他指出,反应过度的情况与反应不足的情况出现的频率一样高,并指出这一特征与市场效率是一致的。根据这种观点,当价格和基本价值平均一致时,市场是有效的,任何偏差都是偶然的。在这方面,平均异常收益为零;然而,随机波动会在两个方向上产生非零偏差(异常)。

Fama(1998)对上面讨论的一些关键文章进行了批判性评估,包括De Bondt和Thaler (1985);杰加迪什和提特曼(1993年);Barberis, Shleifer和Vishny (1998);Daniel, Hirshleifer, and Subrahmanyam(1998)。法玛的批评性质各不相同。他指出Fama和French $(1992,1996)$三因素风险模型可以解释De Bondt和Thaler(1985)和Ikenberry, Lakonishok, and Vermaelen(1995)报告的效应。因此,他认为有效市场范式可以适应这些影响。他认为Barberis, Shleifer, and Vishny(1998)和Daniel, Hirshleifer, and Subrahmanyam(1998)缺乏稳健性,认为这些理论可能解释了他们建立的异常现象,但无法解释其他具有相似特征的理论。Fama发现,对有效市场假说提出最重大挑战的研究与收入公布漂移有关(Bernard and Thomas, 1990)。关于财报公布偏差的发现是,财报意外似乎是正自相关的,这表明分析师对财报反应不足。此外,相关的股票回报出现了漂移,表明投资者整体反应不足。值得注意的是,这种漂移是短期的,随后是长期的逆转。

金融代写|投资组合代写Portfolio Theory代考 请认准exambang™. exambang™为您的留学生涯保驾护航。

微观经济学代写

微观经济学是主流经济学的一个分支,研究个人和企业在做出有关稀缺资源分配的决策时的行为以及这些个人和企业之间的相互作用。my-assignmentexpert™ 为您的留学生涯保驾护航 在数学Mathematics作业代写方面已经树立了自己的口碑, 保证靠谱, 高质且原创的数学Mathematics代写服务。我们的专家在图论代写Graph Theory代写方面经验极为丰富,各种图论代写Graph Theory相关的作业也就用不着 说。

线性代数代写

线性代数是数学的一个分支,涉及线性方程,如:线性图,如:以及它们在向量空间和通过矩阵的表示。线性代数是几乎所有数学领域的核心。

博弈论代写

现代博弈论始于约翰-冯-诺伊曼(John von Neumann)提出的两人零和博弈中的混合策略均衡的观点及其证明。冯-诺依曼的原始证明使用了关于连续映射到紧凑凸集的布劳威尔定点定理,这成为博弈论和数学经济学的标准方法。在他的论文之后,1944年,他与奥斯卡-莫根斯特恩(Oskar Morgenstern)共同撰写了《游戏和经济行为理论》一书,该书考虑了几个参与者的合作游戏。这本书的第二版提供了预期效用的公理理论,使数理统计学家和经济学家能够处理不确定性下的决策。

微积分代写

微积分,最初被称为无穷小微积分或 “无穷小的微积分”,是对连续变化的数学研究,就像几何学是对形状的研究,而代数是对算术运算的概括研究一样。

它有两个主要分支,微分和积分;微分涉及瞬时变化率和曲线的斜率,而积分涉及数量的累积,以及曲线下或曲线之间的面积。这两个分支通过微积分的基本定理相互联系,它们利用了无限序列和无限级数收敛到一个明确定义的极限的基本概念 。

计量经济学代写

什么是计量经济学?

计量经济学是统计学和数学模型的定量应用,使用数据来发展理论或测试经济学中的现有假设,并根据历史数据预测未来趋势。它对现实世界的数据进行统计试验,然后将结果与被测试的理论进行比较和对比。

根据你是对测试现有理论感兴趣,还是对利用现有数据在这些观察的基础上提出新的假设感兴趣,计量经济学可以细分为两大类:理论和应用。那些经常从事这种实践的人通常被称为计量经济学家。

Matlab代写

MATLAB 是一种用于技术计算的高性能语言。它将计算、可视化和编程集成在一个易于使用的环境中,其中问题和解决方案以熟悉的数学符号表示。典型用途包括:数学和计算算法开发建模、仿真和原型制作数据分析、探索和可视化科学和工程图形应用程序开发,包括图形用户界面构建MATLAB 是一个交互式系统,其基本数据元素是一个不需要维度的数组。这使您可以解决许多技术计算问题,尤其是那些具有矩阵和向量公式的问题,而只需用 C 或 Fortran 等标量非交互式语言编写程序所需的时间的一小部分。MATLAB 名称代表矩阵实验室。MATLAB 最初的编写目的是提供对由 LINPACK 和 EISPACK 项目开发的矩阵软件的轻松访问,这两个项目共同代表了矩阵计算软件的最新技术。MATLAB 经过多年的发展,得到了许多用户的投入。在大学环境中,它是数学、工程和科学入门和高级课程的标准教学工具。在工业领域,MATLAB 是高效研究、开发和分析的首选工具。MATLAB 具有一系列称为工具箱的特定于应用程序的解决方案。对于大多数 MATLAB 用户来说非常重要,工具箱允许您学习和应用专业技术。工具箱是 MATLAB 函数(M 文件)的综合集合,可扩展 MATLAB 环境以解决特定类别的问题。可用工具箱的领域包括信号处理、控制系统、神经网络、模糊逻辑、小波、仿真等。